The Local Lowdown: May 2024

Michelle Kim | June 11, 2024

Michelle Kim | June 11, 2024

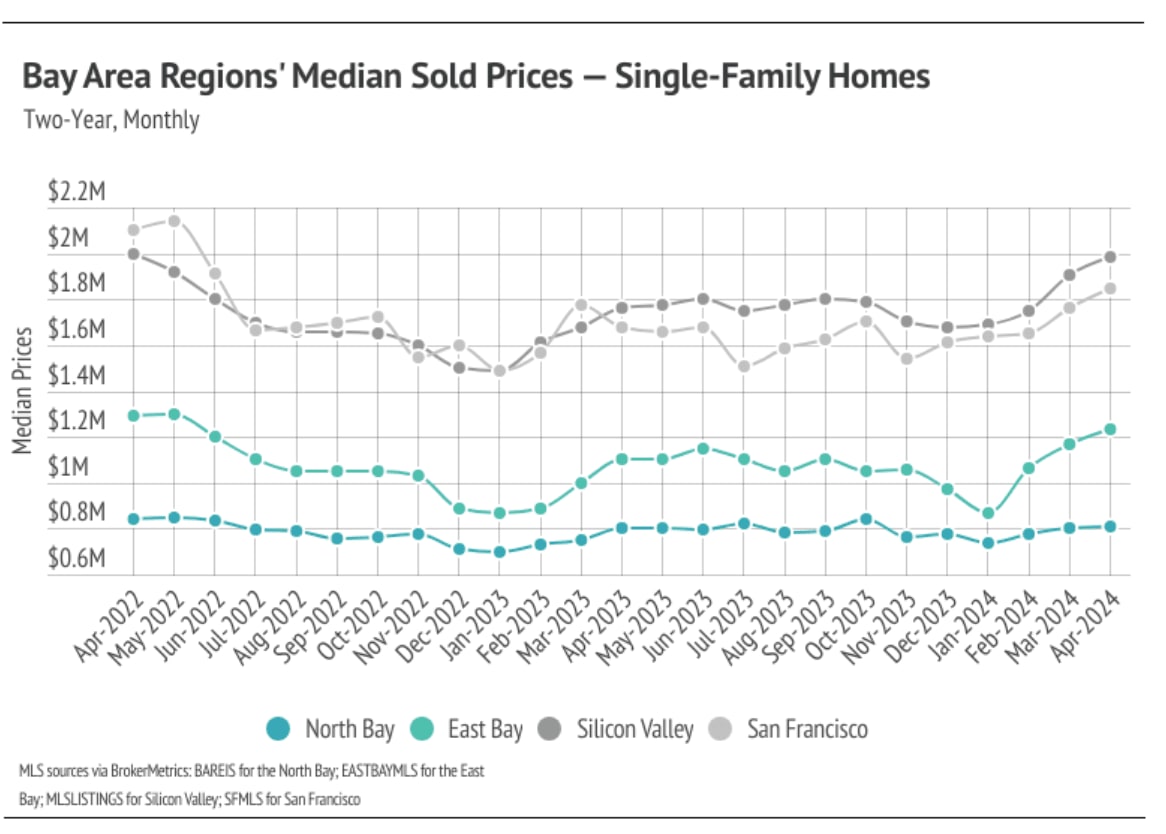

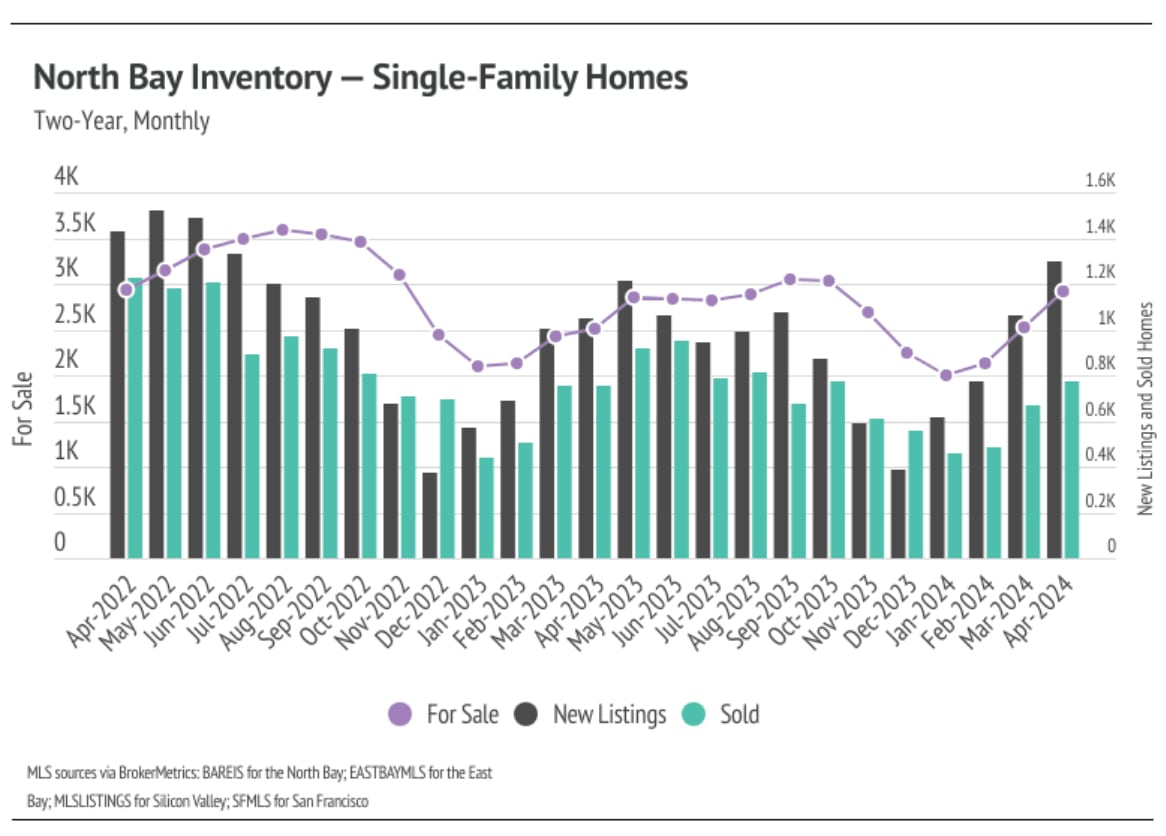

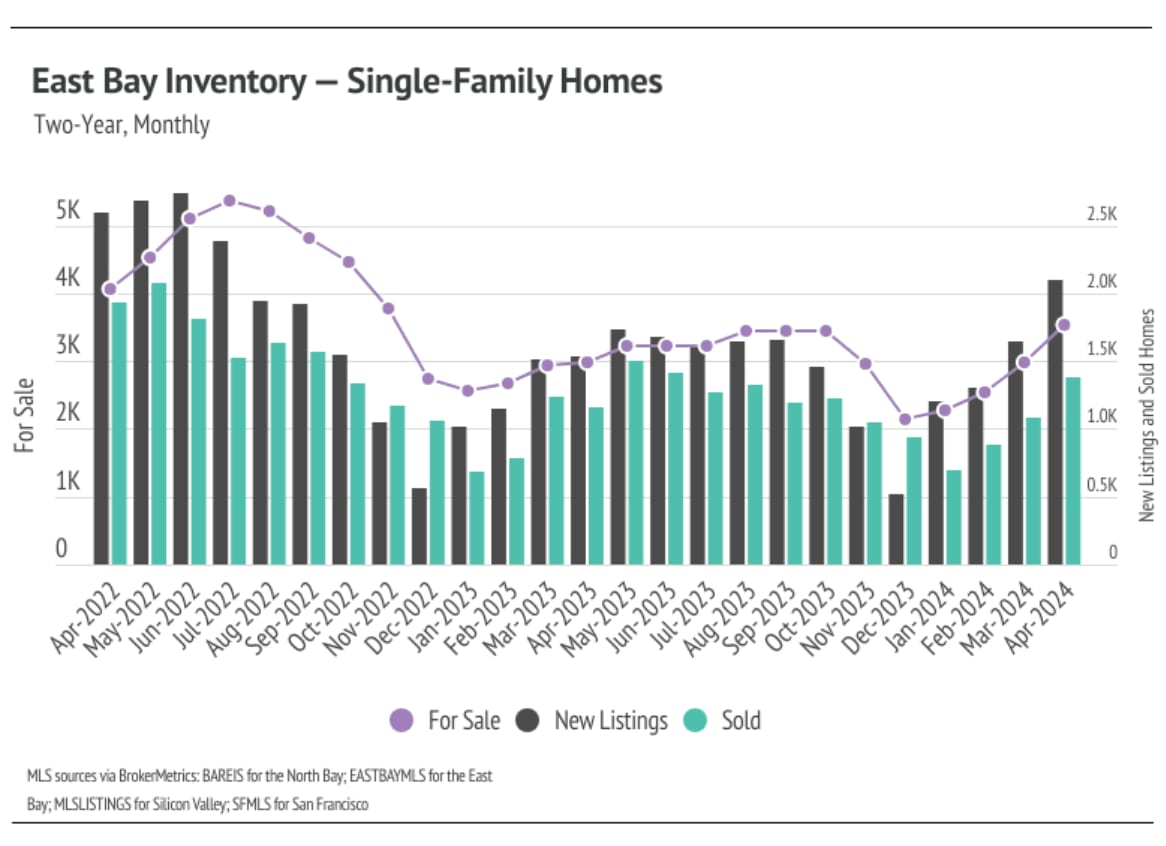

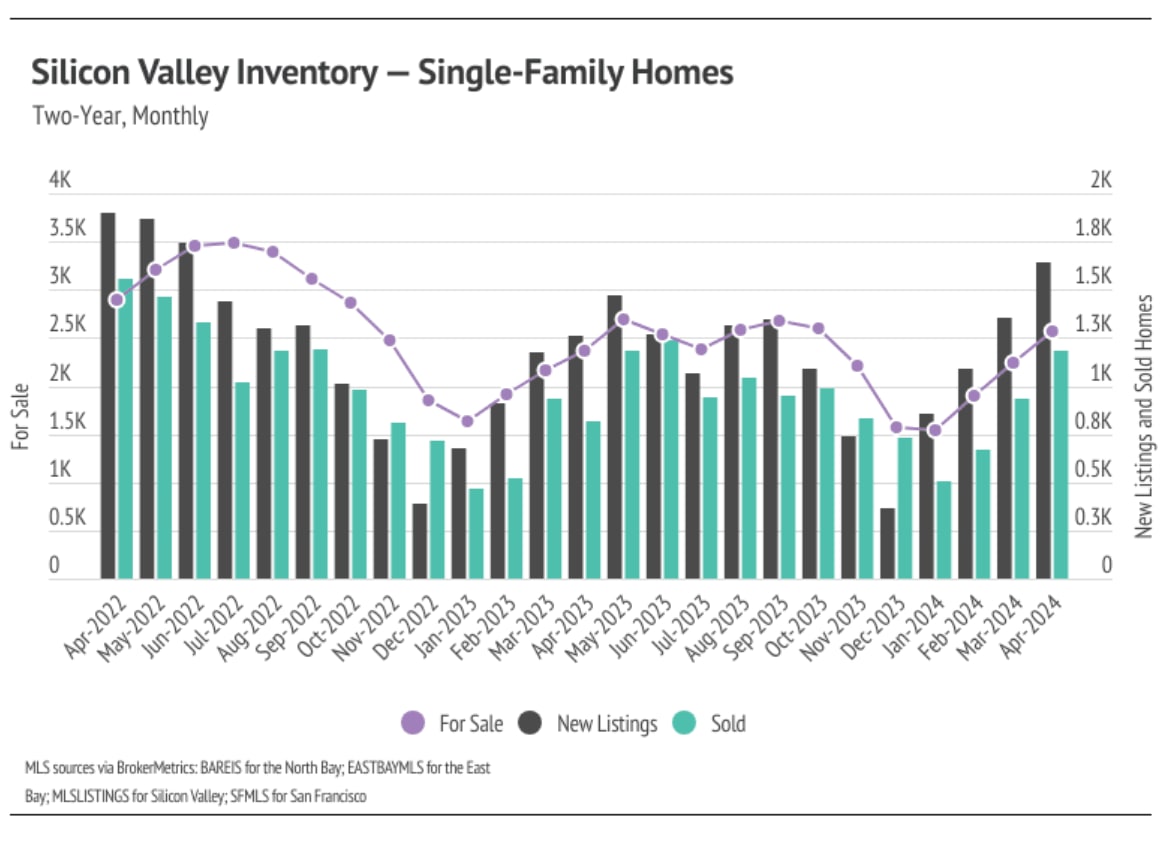

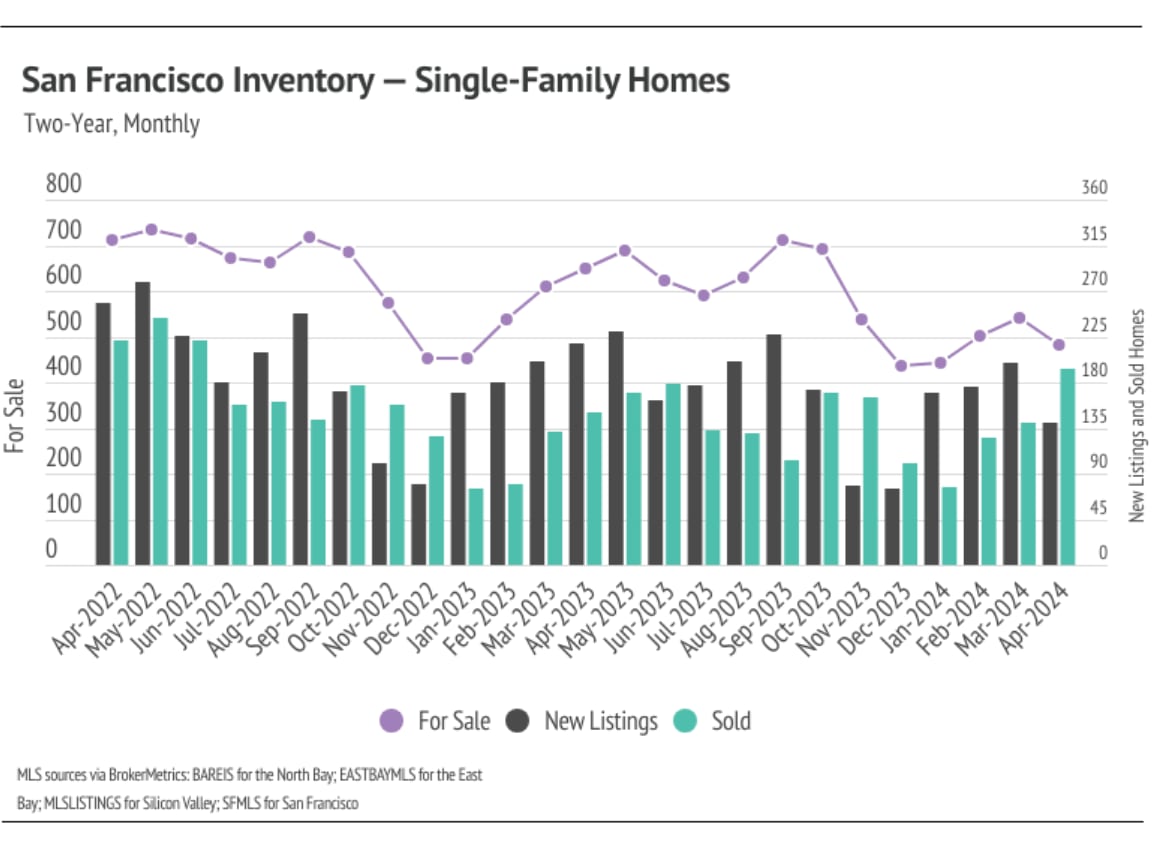

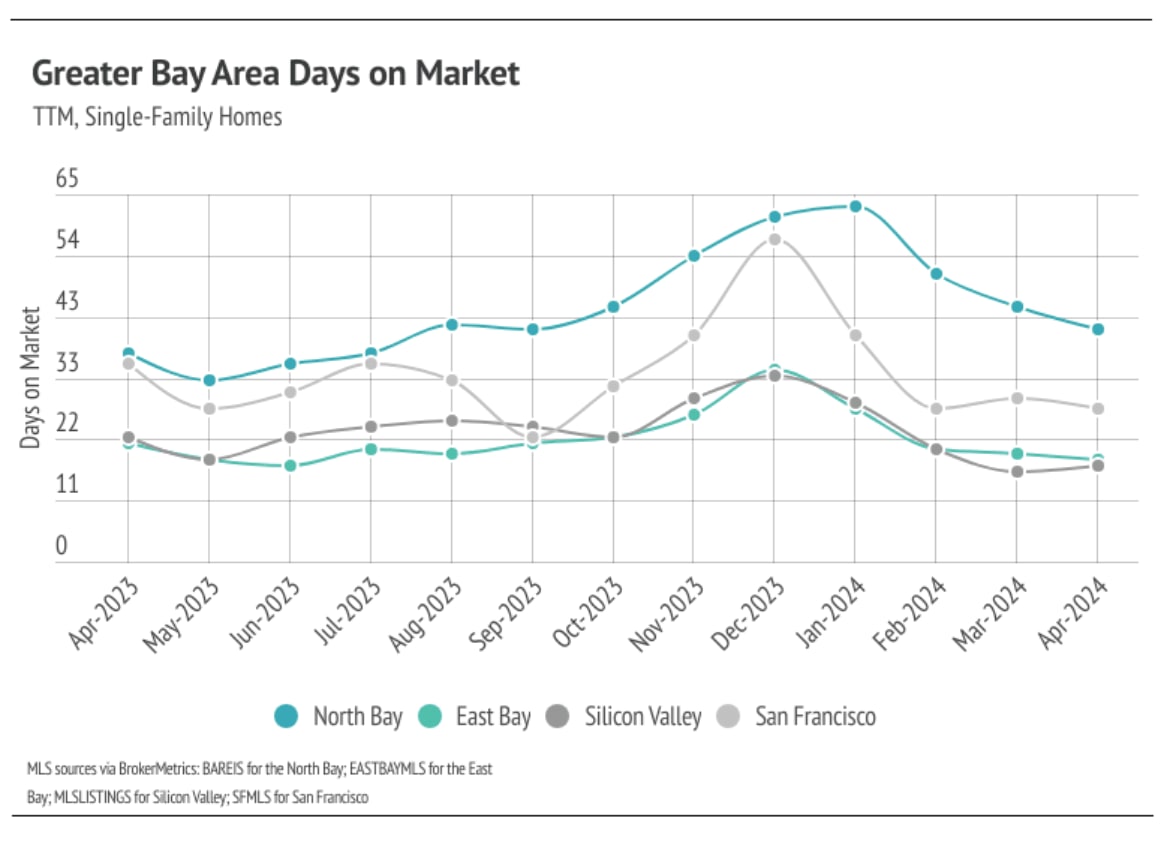

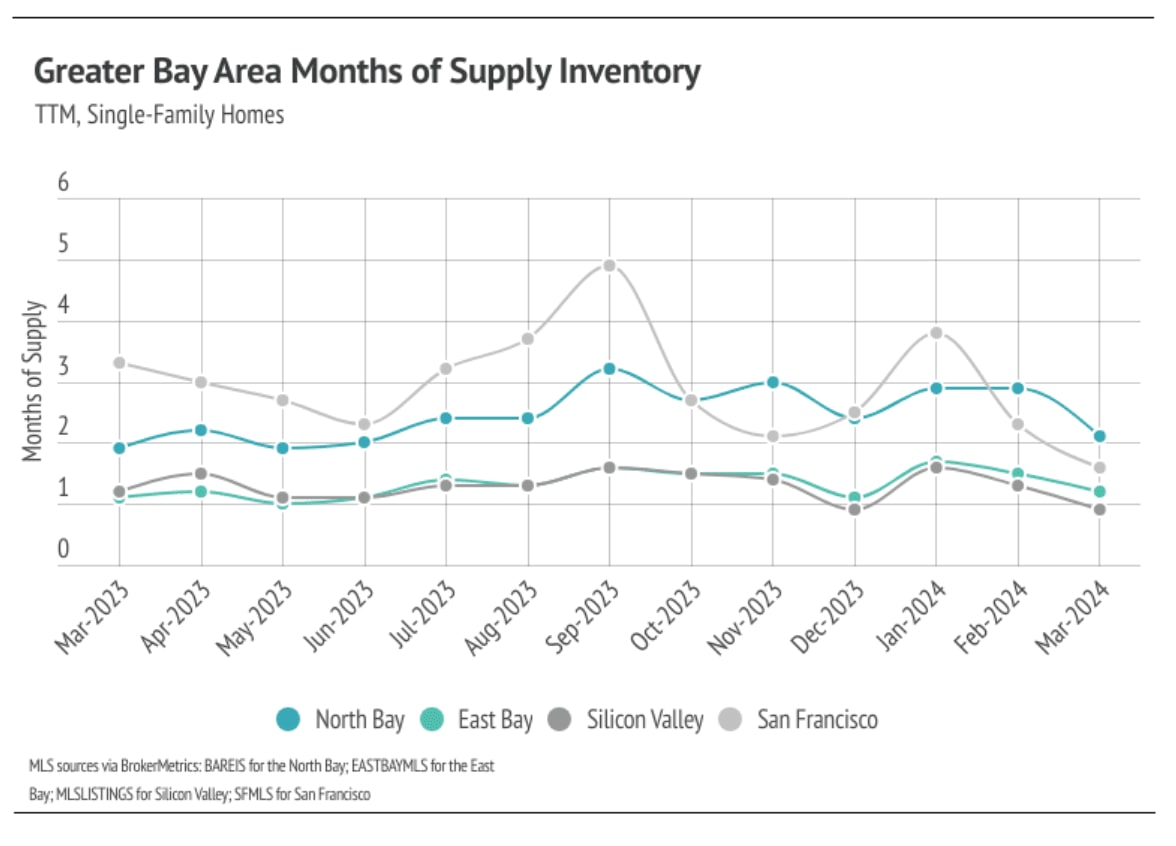

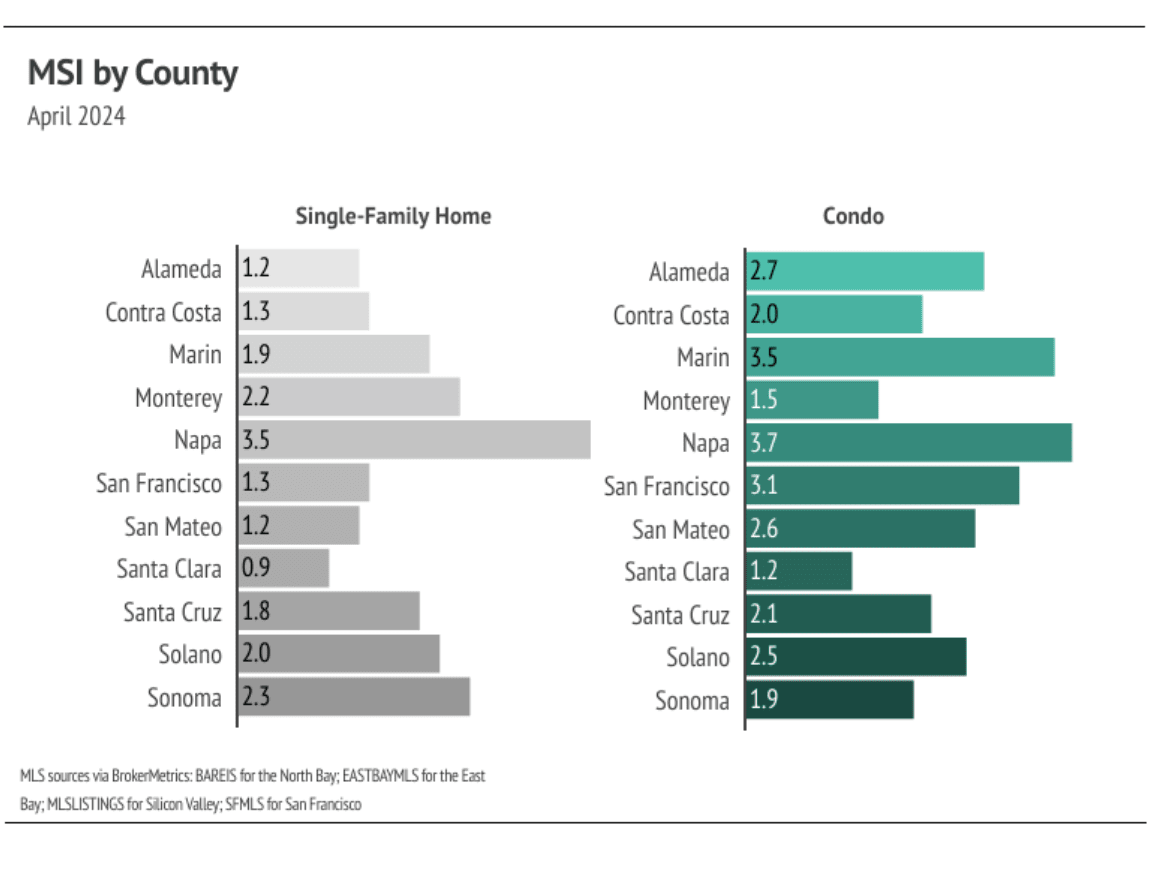

Since the start of 2023, single-family home inventory has followed fairly typical seasonal trends, but at significantly depressed levels. Low inventory and fewer new listings have slowed the market considerably. Typically, inventory peaks in July or August and declines through December or January, but the lack of new listings prevented meaningful inventory growth. New listings have been exceptionally low, so the little inventory growth in 2023 was driven by softening demand. In December 2023, inventory and sales dropped. However, more new listings have come to the market in 2024, which has driven the significant increase in sales so far this year. The market is already looking healthier, and we expect more new listings and sales in Q2 2024.

Stay up to date on the latest real estate trends.

Michelle Kim | May 22, 2026

A closer look at how buyers are comparing condos and single-family homes in the 2026 San Francisco housing market based on lifestyle, budget, and long-term goals.

Michelle Kim | May 15, 2026

A closer look at why San Francisco buyers continue to prioritize neighborhoods near Golden Gate Park for outdoor access, walkability, and long-term livability.

Michelle Kim | May 8, 2026

A look at how Mosaik Real Estate supports Bay Area buyers and sellers through multilingual communication and local market expertise.

Michelle Kim | May 1, 2026

A closer look at San Francisco housing market trends in 2026 and what buyers and sellers should expect moving forward.

Michelle Kim | May 1, 2026

Quick Take: Median home sale prices ticked up slightly on both a month-over-month and year-over-year basis in February, continuing the holding pattern we've seen in re… Read more

Michelle Kim | May 1, 2026

Quick Take: Median sale prices rebounded in Sonoma County with a 1.16% year-over-year gain, while Napa County continued to struggle with a 10.61% decline. Inventory re… Read more

You’ve got questions and we can’t wait to answer them.