The Local Lowdown: July 2024

Michelle Kim | July 26, 2024

Michelle Kim | July 26, 2024

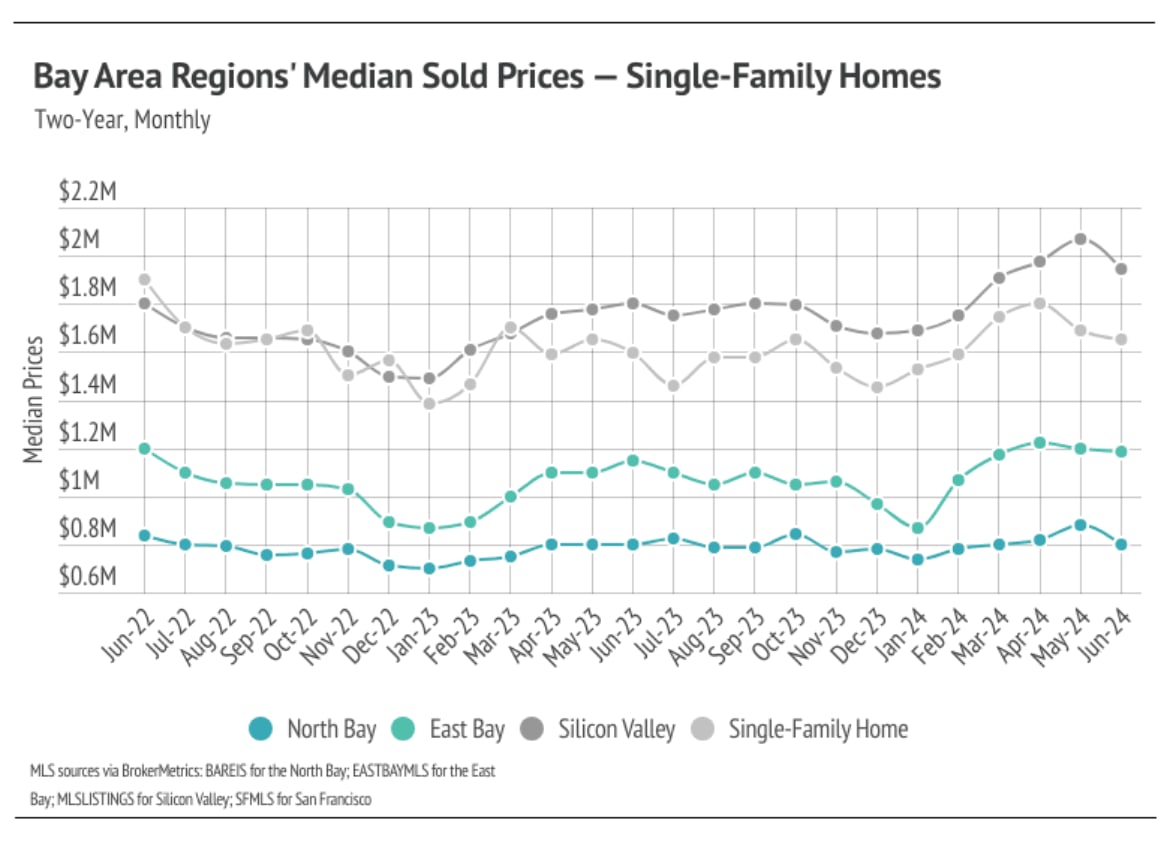

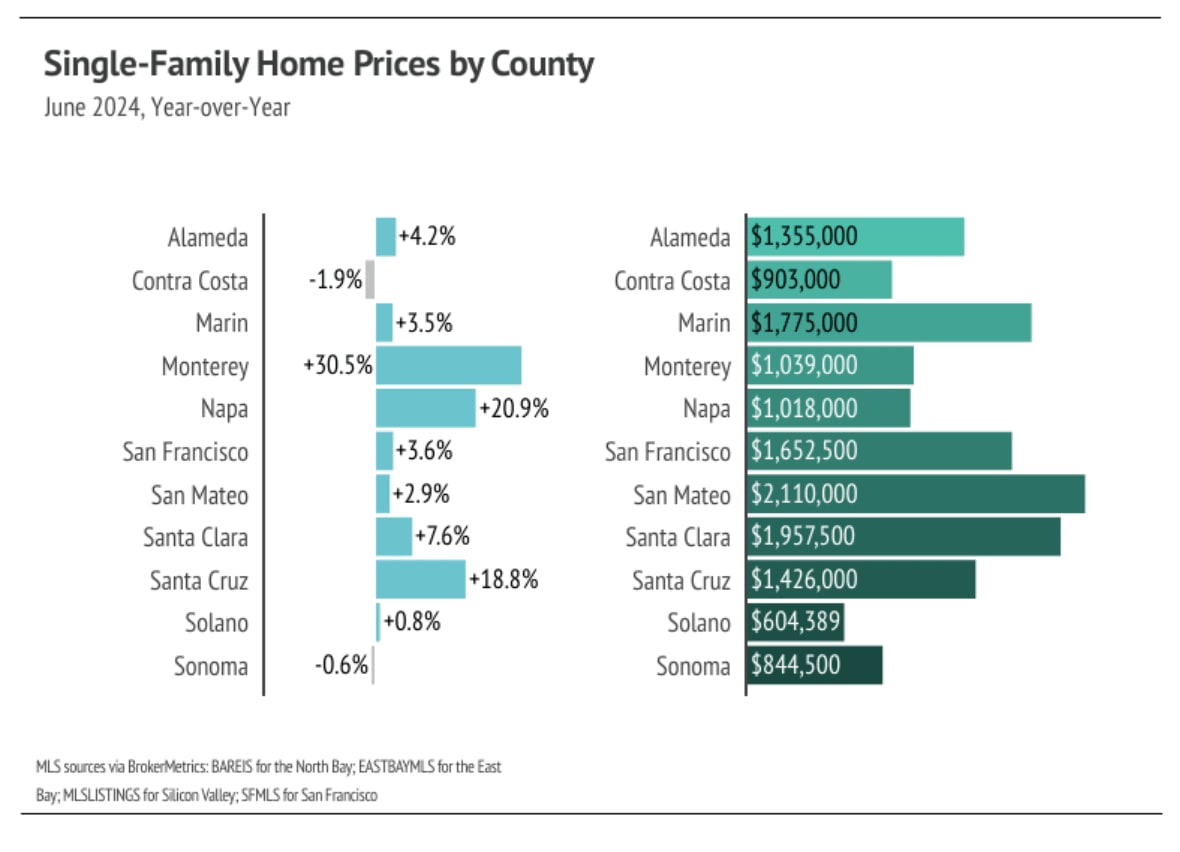

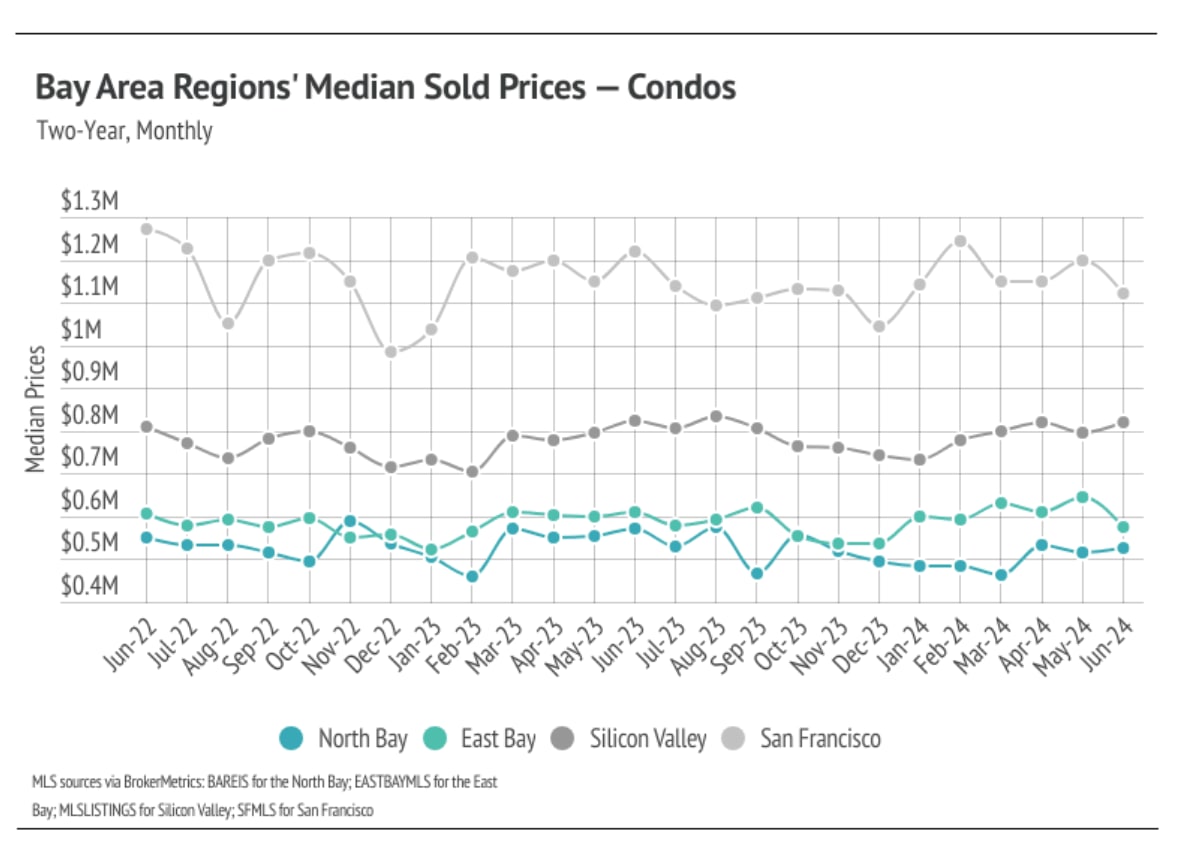

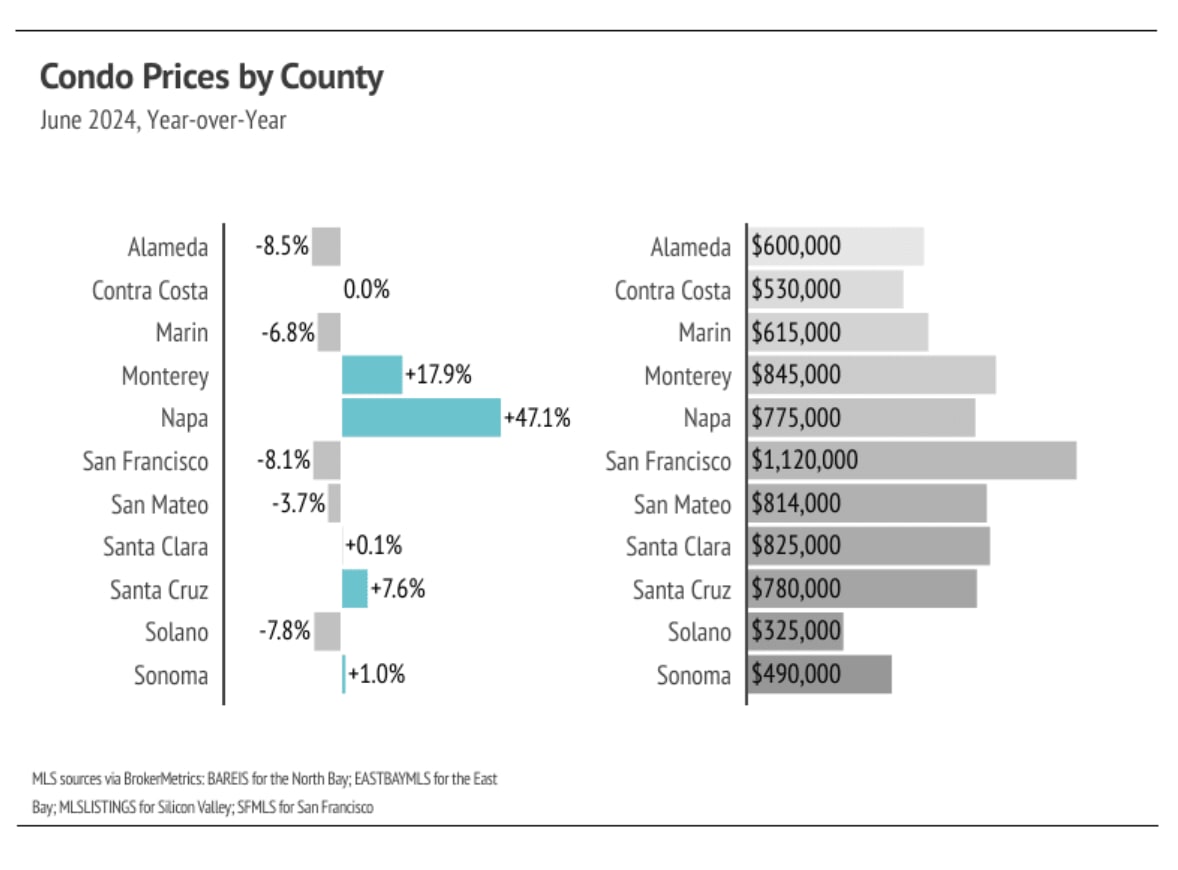

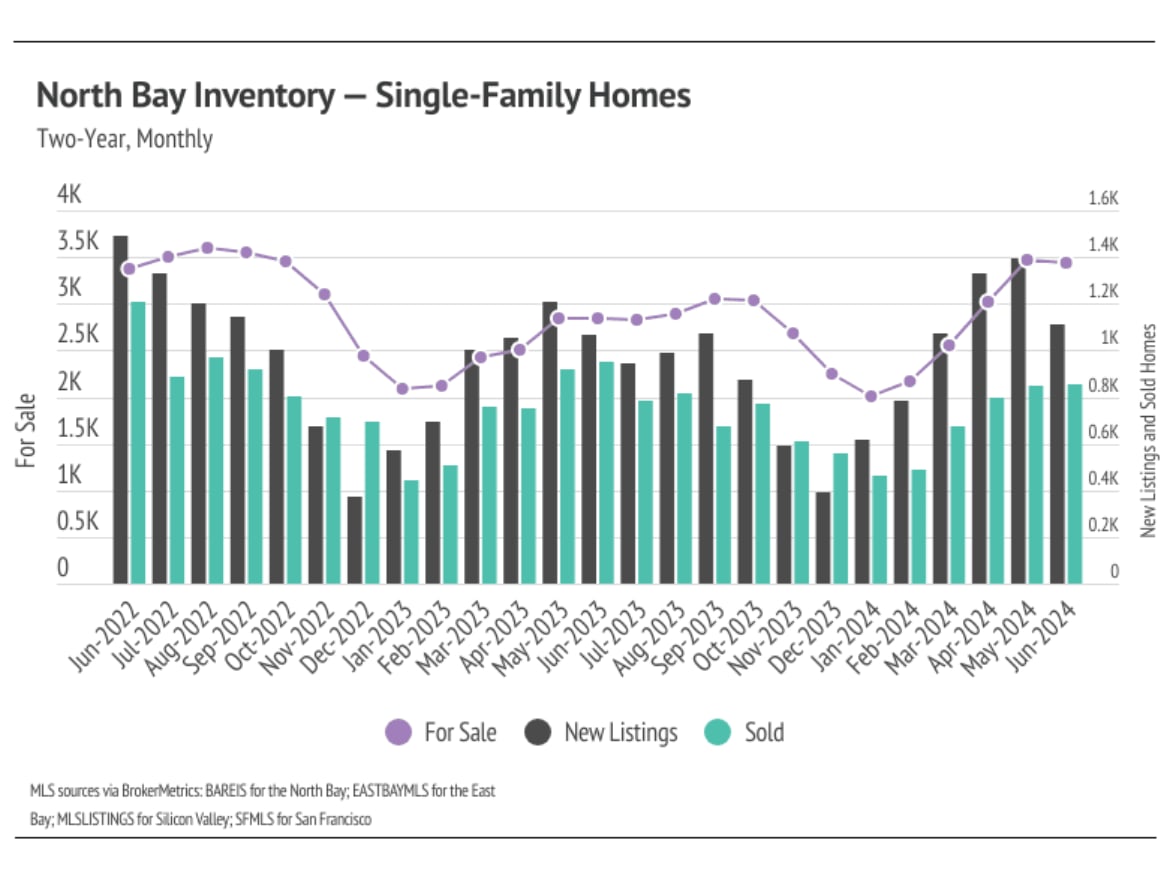

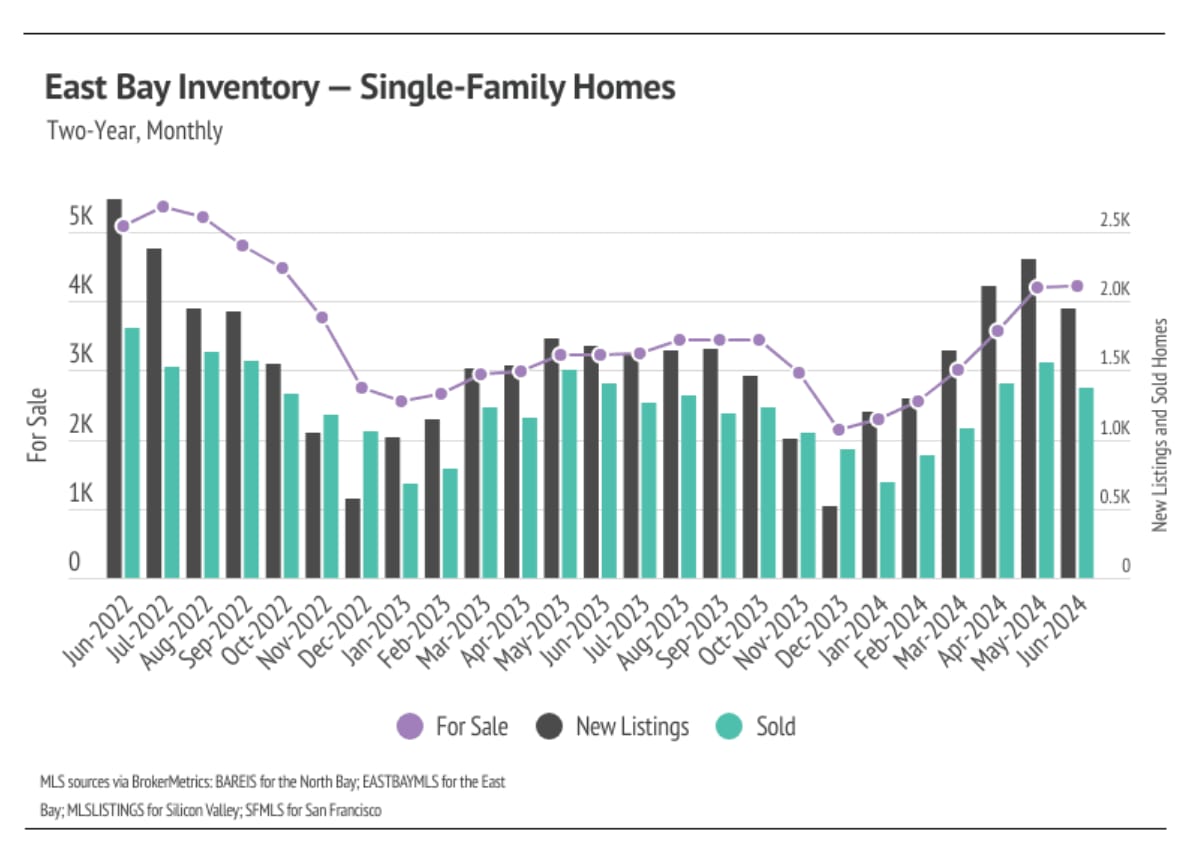

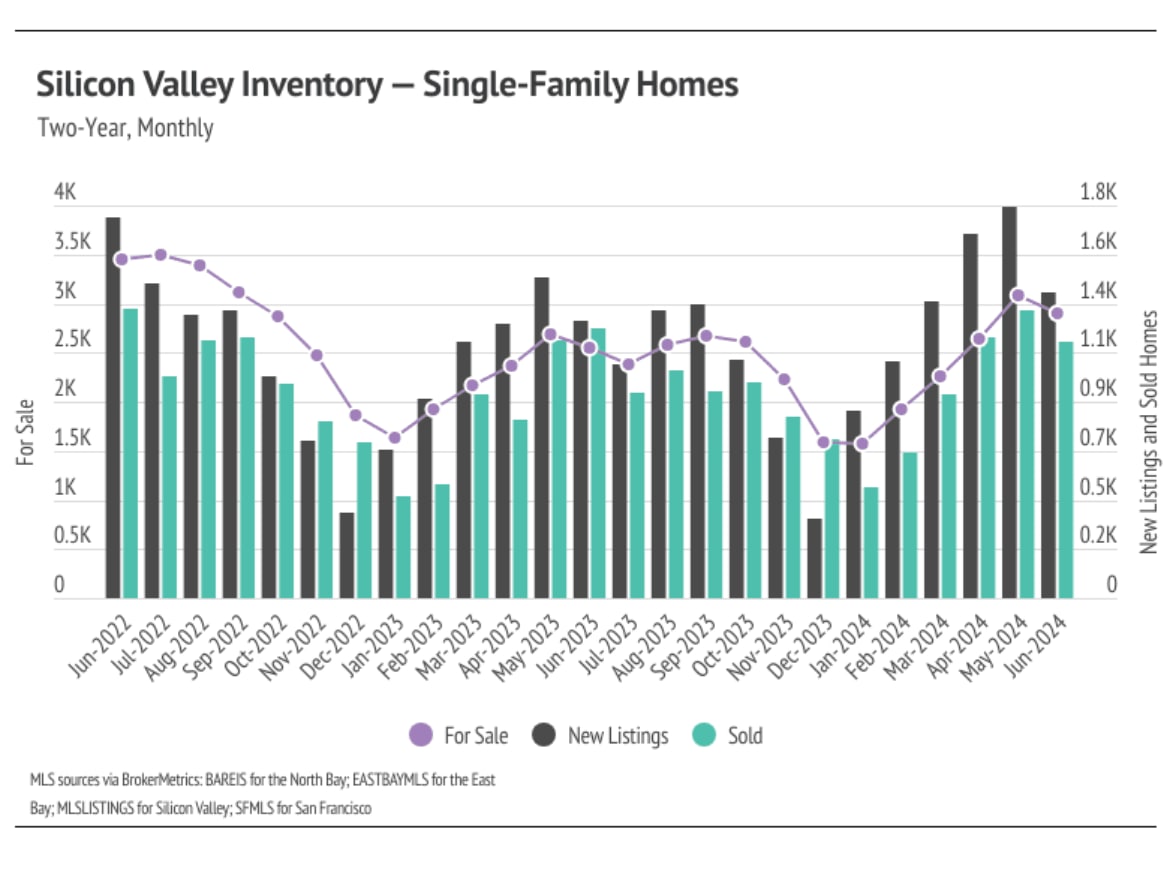

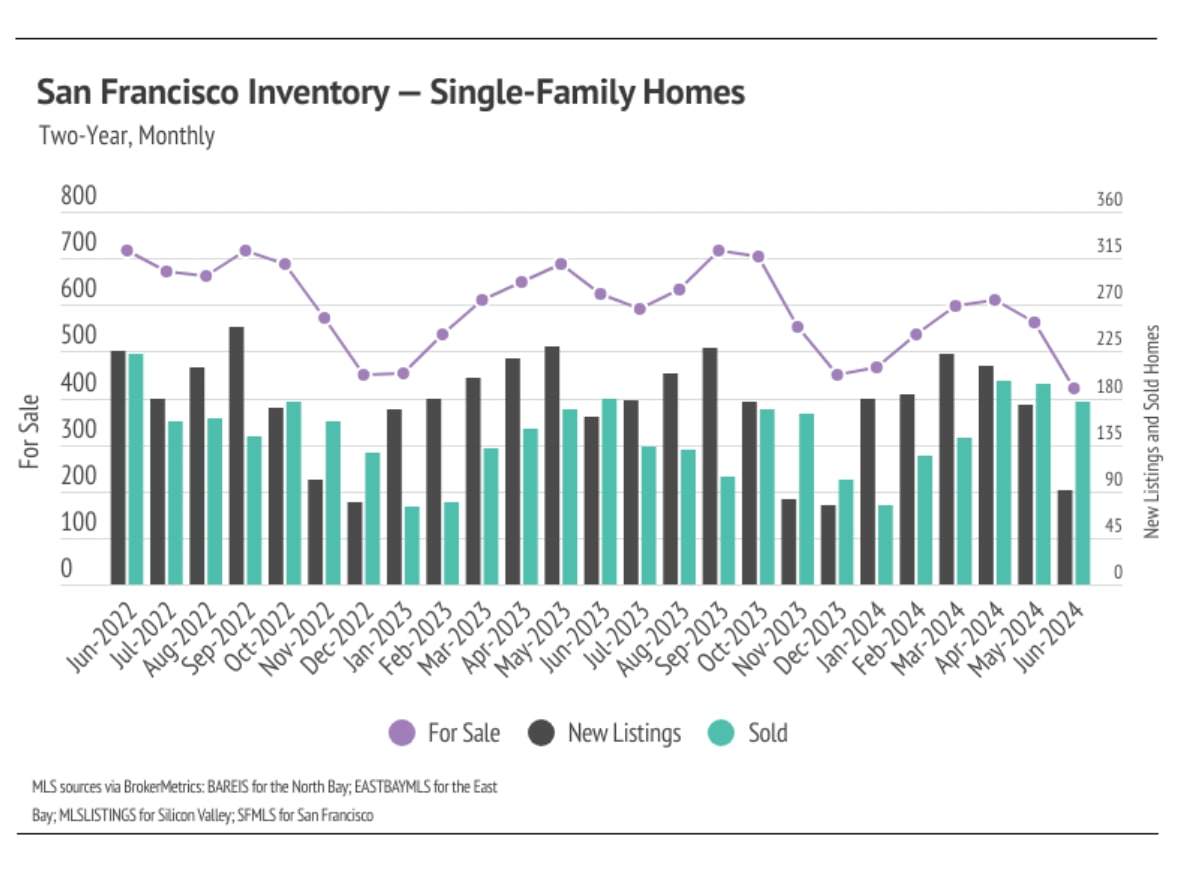

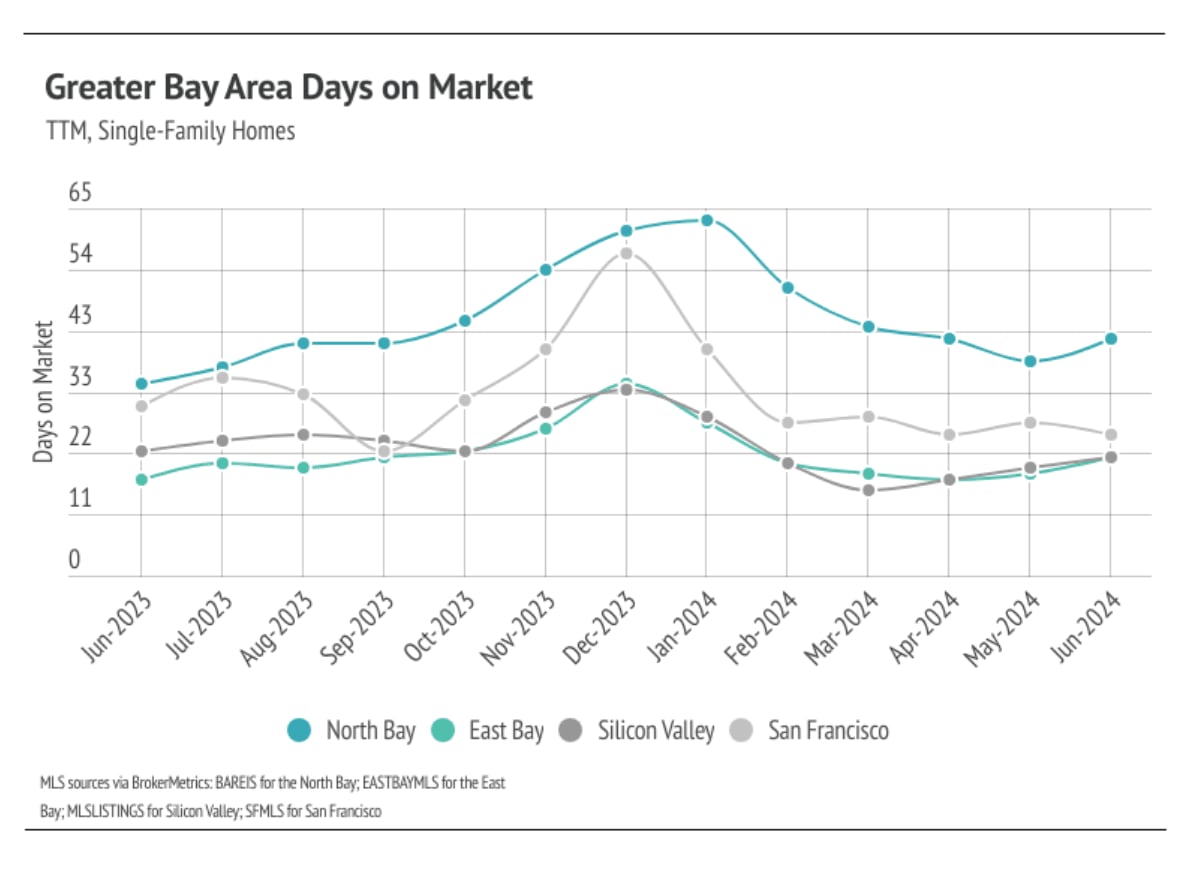

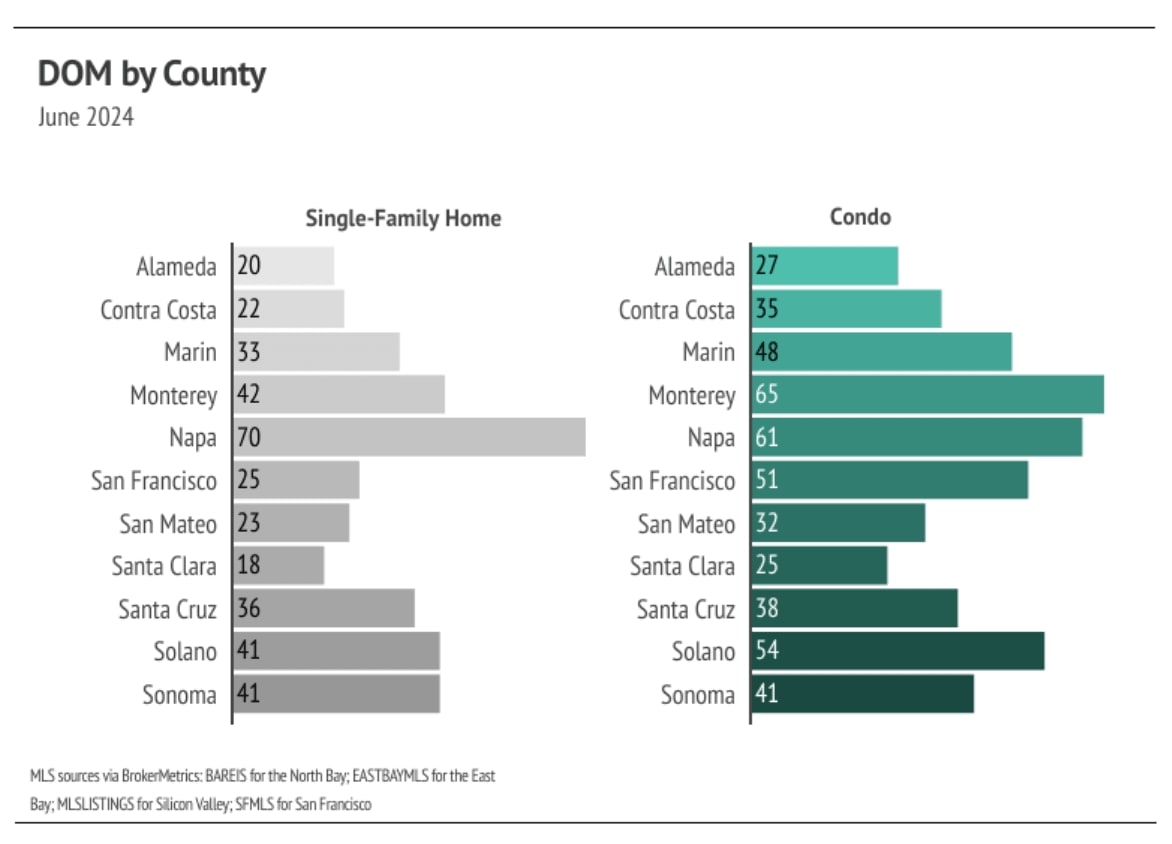

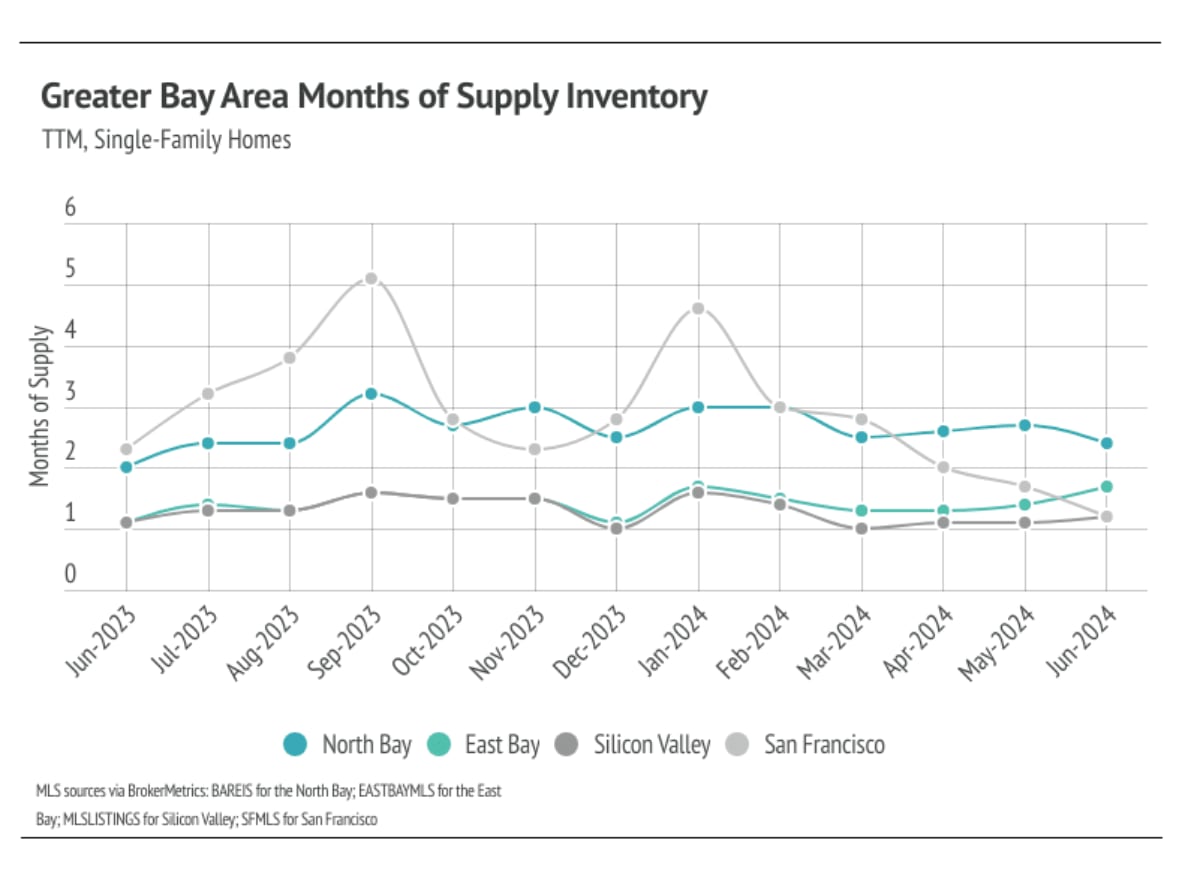

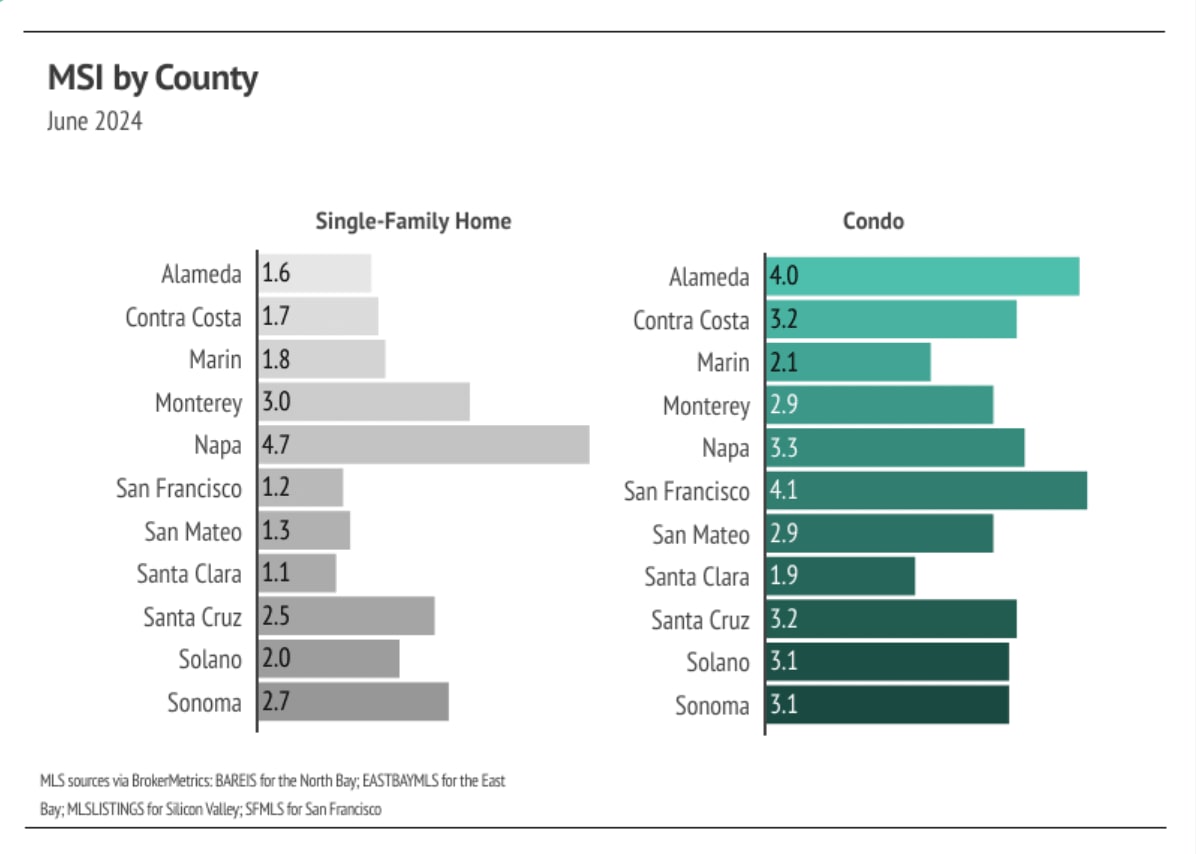

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The Bay Area markets tend to favor sellers, which is reflected in their low MSIs. San Francisco MSI is notable for its variability over the past year, oscillating from buyers’ to sellers’ markets twice over the course of 12 months. Currently, MSI is below three months of supply (a sellers’ market) in every Bay Area county, except for single-family homes in Napa, which favor buyers, and condos in the North Bay, East Bay, and San Francisco, which are now balanced.

Stay up to date on the latest real estate trends.

Michelle Kim | May 29, 2026

A closer look at why more San Francisco buyers are prioritizing walkability, local cafés, restaurants, parks, and lifestyle when choosing the right neighborhood.

Michelle Kim | May 22, 2026

A closer look at how buyers are comparing condos and single-family homes in the 2026 San Francisco housing market based on lifestyle, budget, and long-term goals.

Michelle Kim | May 15, 2026

A closer look at why San Francisco buyers continue to prioritize neighborhoods near Golden Gate Park for outdoor access, walkability, and long-term livability.

Michelle Kim | May 8, 2026

A look at how Mosaik Real Estate supports Bay Area buyers and sellers through multilingual communication and local market expertise.

Michelle Kim | May 1, 2026

A closer look at San Francisco housing market trends in 2026 and what buyers and sellers should expect moving forward.

Michelle Kim | May 1, 2026

Quick Take: Median home sale prices ticked up slightly on both a month-over-month and year-over-year basis in February, continuing the holding pattern we've seen in re… Read more

You’ve got questions and we can’t wait to answer them.