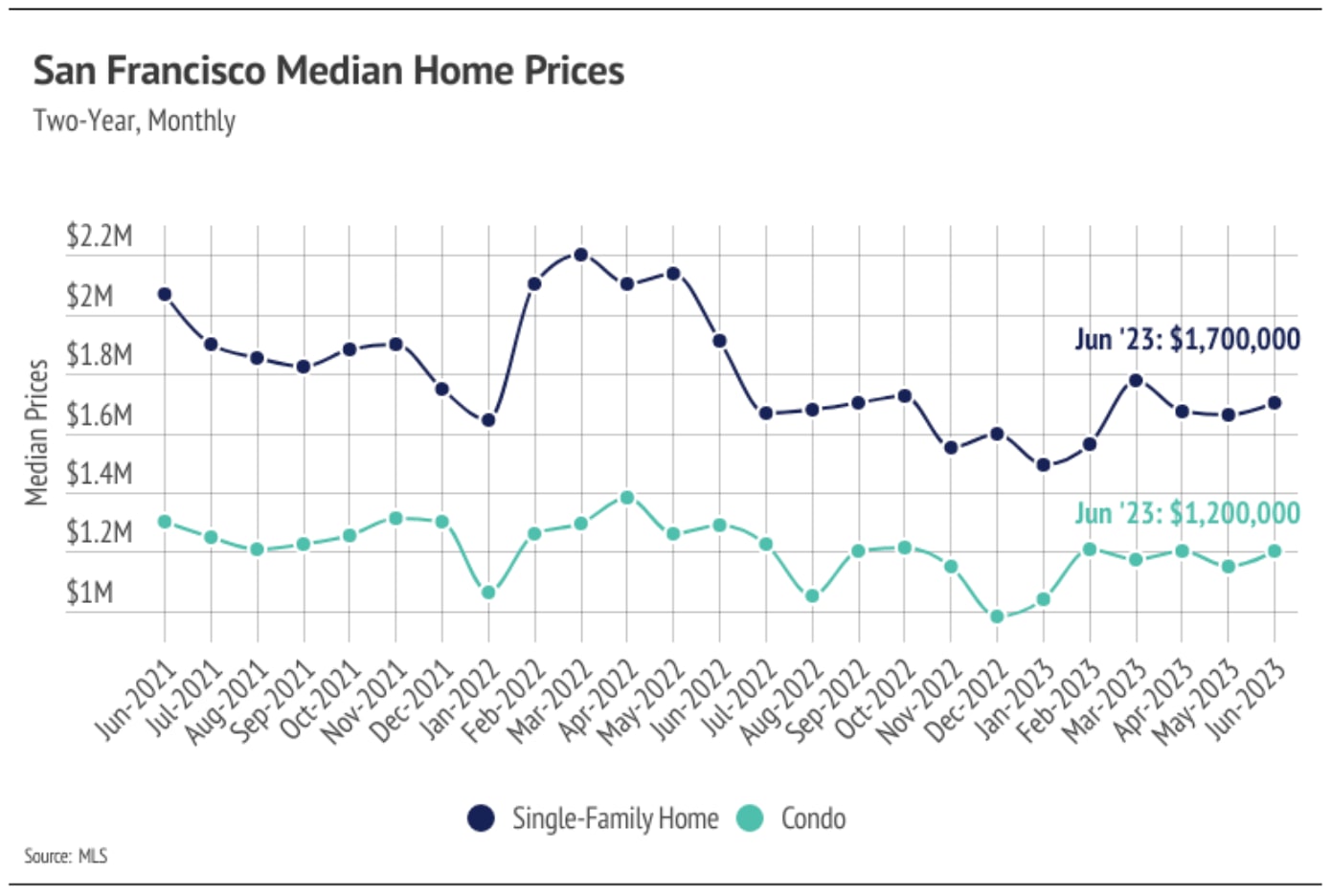

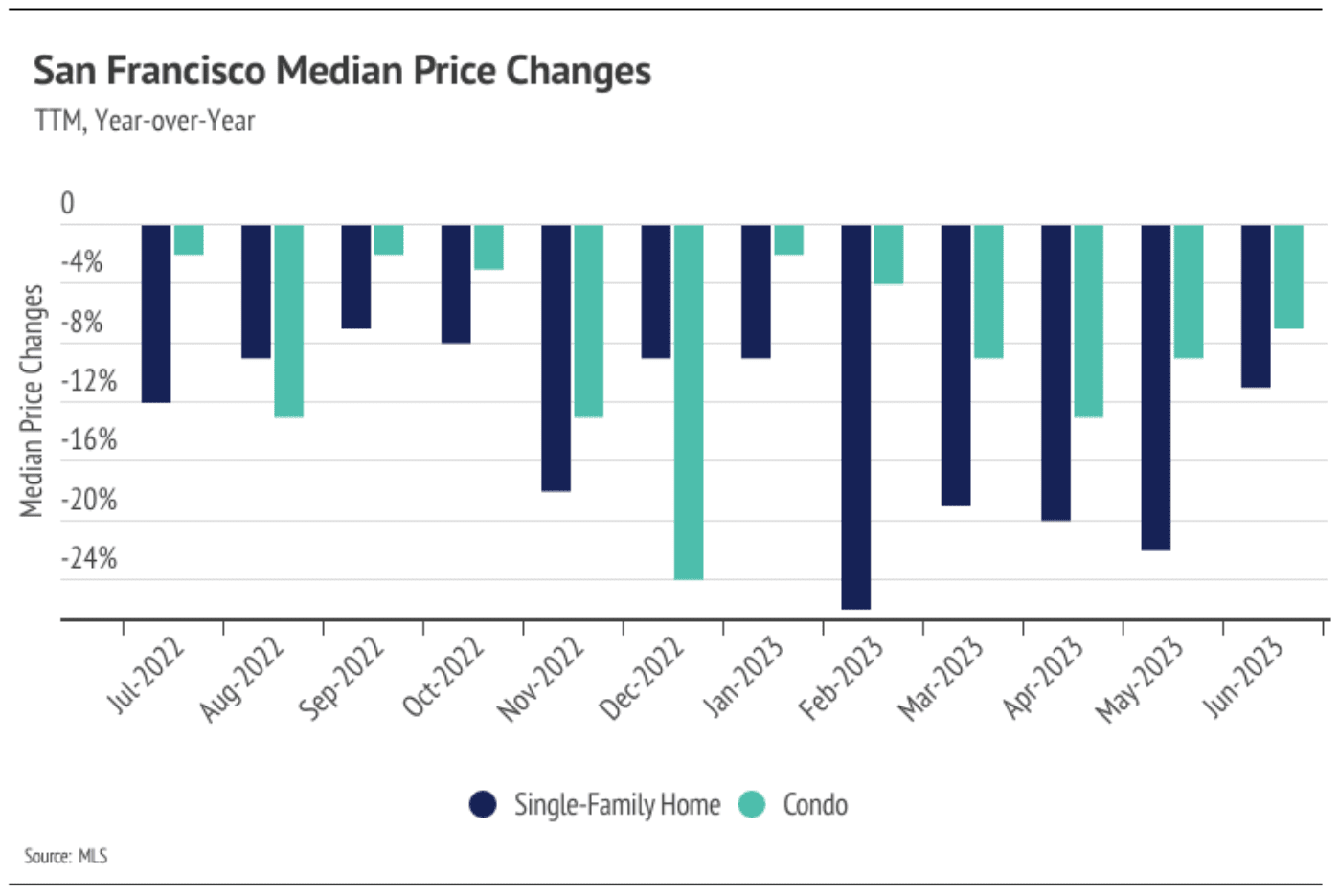

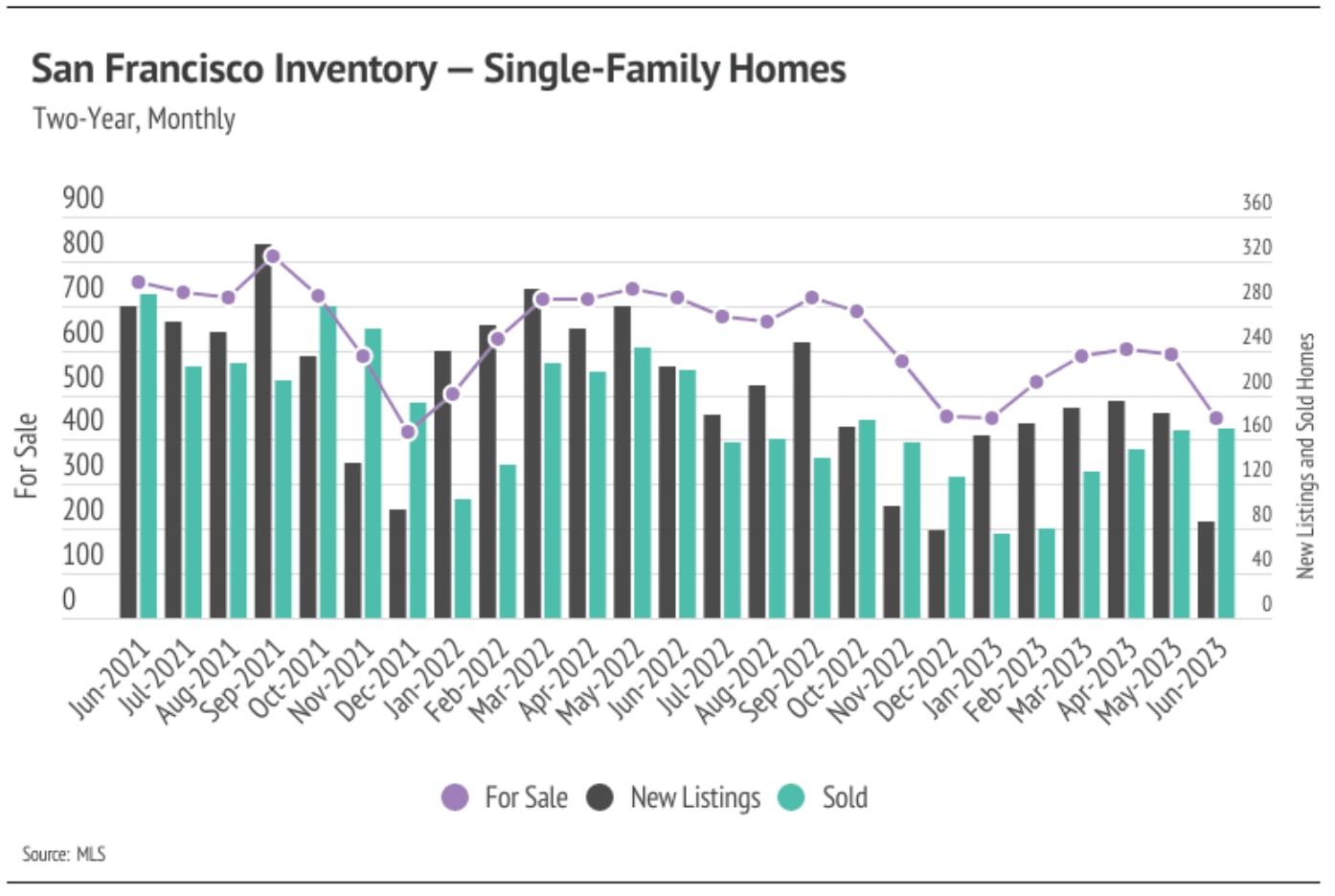

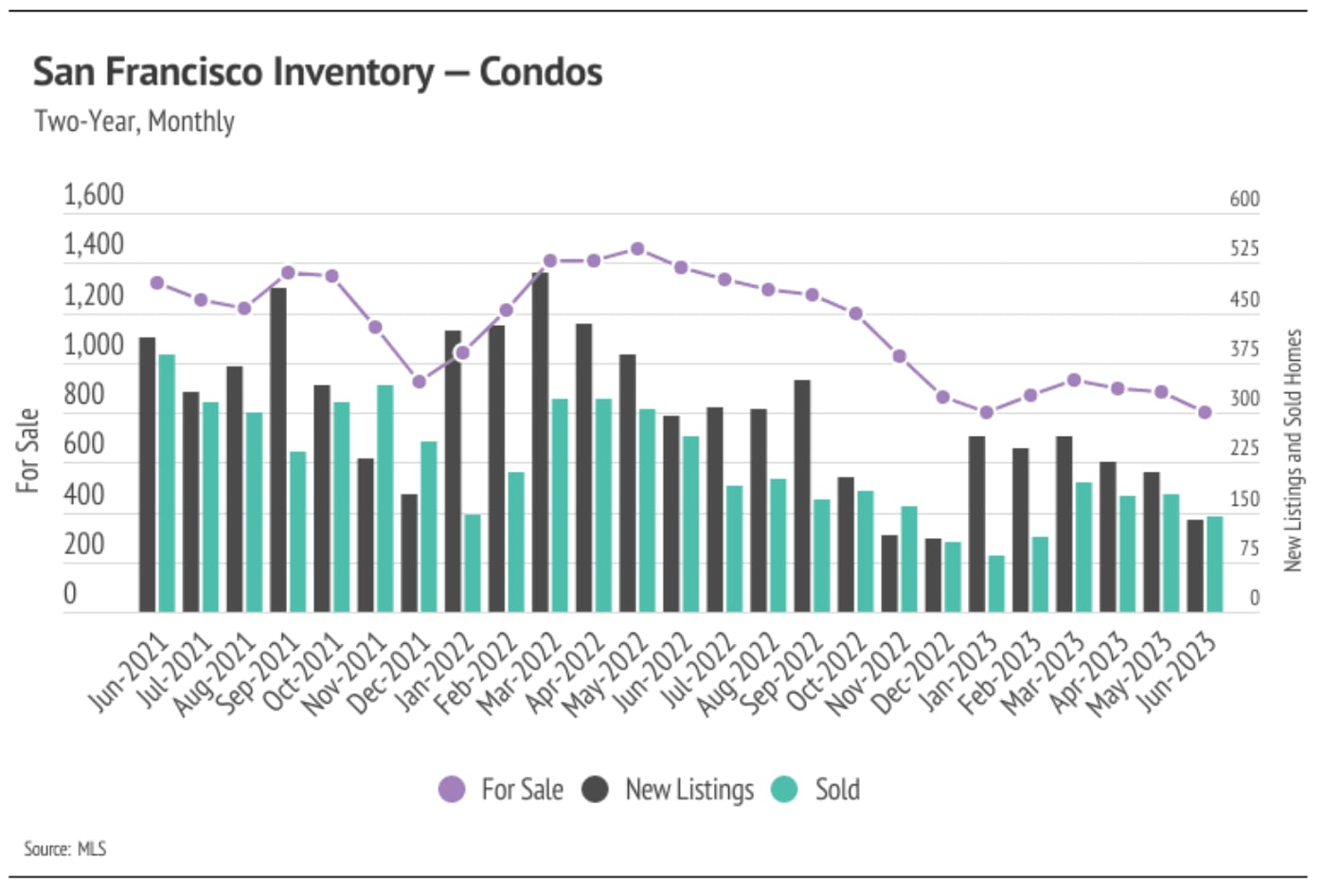

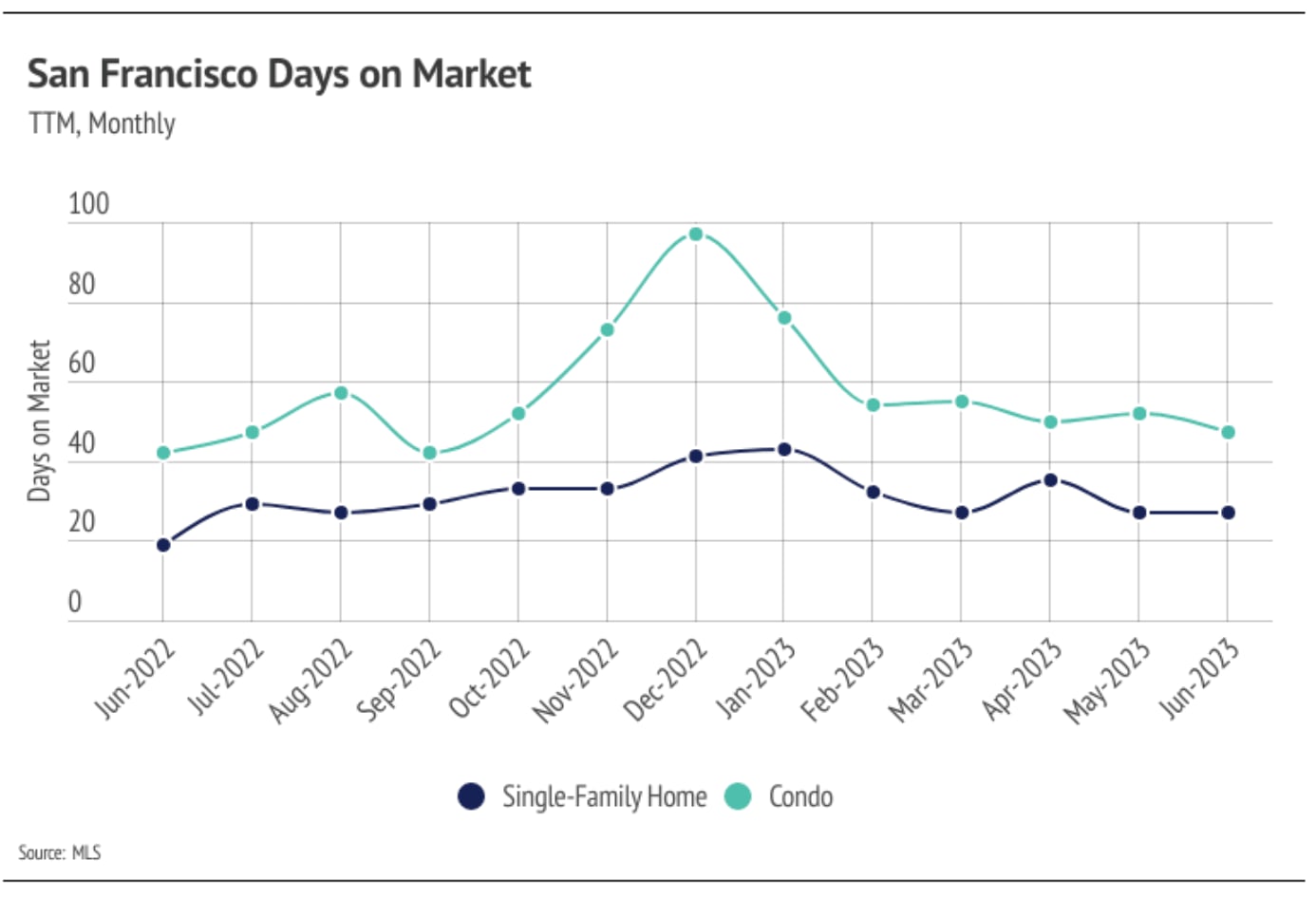

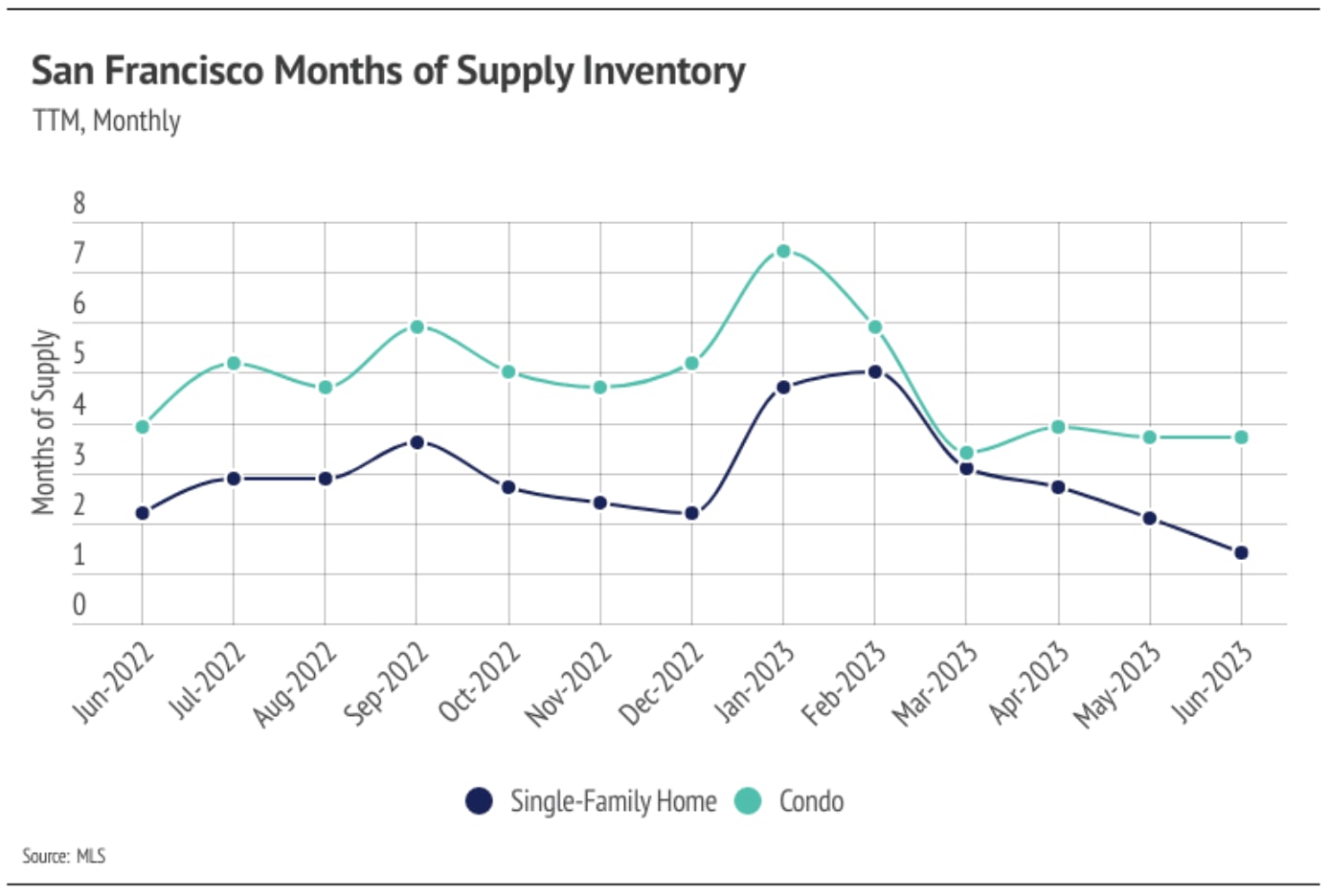

The Local Lowdown: August 2023

Michelle Kim | August 1, 2023

Michelle Kim | August 1, 2023

Stay up to date on the latest real estate trends.

Michelle Kim | April 24, 2026

A closer look at San Mateo real estate, lifestyle, and what makes this Peninsula city a practical choice for Bay Area buyers.

Michelle Kim | April 17, 2026

Exploring Oakland’s walkable neighborhoods, local dining scene, and everyday lifestyle for Bay Area buyers.

Michelle Kim | April 2, 2026

A breakdown of San Francisco districts and how each area differs in lifestyle, housing, and accessibility for buyers.

Michelle Kim | April 1, 2026

Quick Take: Median home sale prices are virtually flat on a year-over-year basis, as the market has settled into a holding pattern despite lower mortgage rates. Invent… Read more

Michelle Kim | April 1, 2026

Quick Take: Median sale prices declined across most of the North Bay in February, with Napa County single-family homes down 20.86% and Marin County down 5.74% on a yea… Read more

Michelle Kim | April 1, 2026

Quick Take: Single-family home prices in Alameda County bounced back to $1.3 million, while condo prices remain mixed with a notable rebound in Contra Costa County. In… Read more

You’ve got questions and we can’t wait to answer them.