South Bay & Peninsula Real Estate Market Report: August 2022

jordan

August 1, 2022

SHARE

The Big Story

To be, or not to be? That is the recession.

Quick Take:

The housing market strongly outperformed inflation and stocks in the first half of 2022 and shows no sign of reversing.

The Fed rate hikes are dampening demand, allowing much-needed inventory to rise, although inventory remains far from the pre-pandemic supply norms.

The economy is slowing, but a recession may not be guaranteed quite yet. Regardless, housing is poised to hold steady or increase in value.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

Rising rates, rising prices, and economic slowdown, but homes still ahead

Economic outlooks seem to change month-to-month, and yet again, we find ourselves in a unique moment in time. The Fed rapidly switched from loose to contractionary monetary policy in March and recently increased the federal funds rate by 0.75% — the biggest increase since 1994. The effects have yet to curb inflation, which is still at a 40-year high (+8.5% CPI year-over-year). On a monthly basis, the Bureau of Labor Statistics (BLS) collects the prices of approximately 94,000 items from a sample of goods and services to calculate the Consumer Price Index (CPI). We didn’t look into everything in the BLS sample, but if you’re like us, it feels like everything we buy is closer to 50–100% higher than it was a year ago, or even several months ago. While prices are rising, the cost to borrow has also gotten more expensive, which is dampening demand.

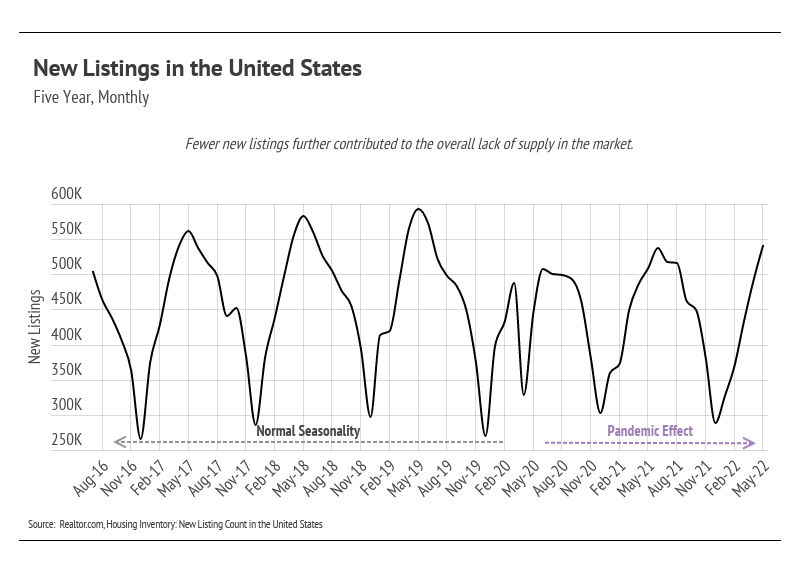

We are starting to see this play out in the housing market. We are noticing more inventory coming to market, coupled with fewer sales. We must, however, provide a caveat: The housing inventory is still historically low. As rates rise, especially as rapidly as they have this year, buyers can get priced out of the market quickly and must reconsider their budgets.

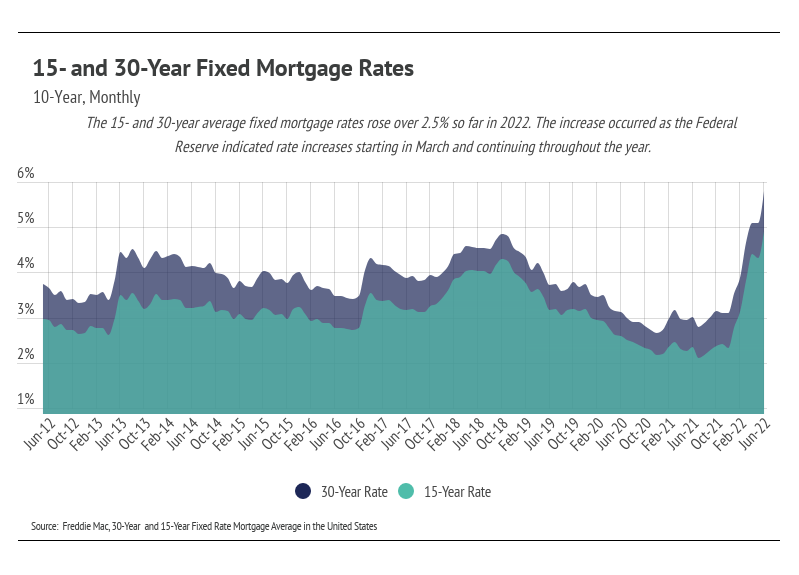

A year ago, the average 30-year mortgage rates hit their lowest levels in history and have more than doubled since then, to 5.81%. Let’s take a look at some numbers to see how assets have performed in the first half of 2022: The S&P 500 declined 21% (the worst first half of the year since 1970), the NASDAQ is down 30%, and Bitcoin and Ethereum have dropped 59% and 71%, respectively. At the same time, U.S. housing prices increased by 15% nationally. Home prices, simply, rarely go down. Even if you weren’t directly affected by the 2006 housing bubble, you likely knew someone who was. One lasting effect of the housing bubble is the perception that home prices decline much like other risk assets, which isn’t the case. Stocks, bonds, and cryptocurrency are fungible assets that allow for large, multiplayer markets. The housing market has only recently become more efficient because of technology, but too many factors play into a home’s value, preventing regular downturns in the market. Large declines in liquid assets do affect demand for homes, though, as people tend to reconsider buying when they feel (and objectively are) less wealthy during dips in those markets.

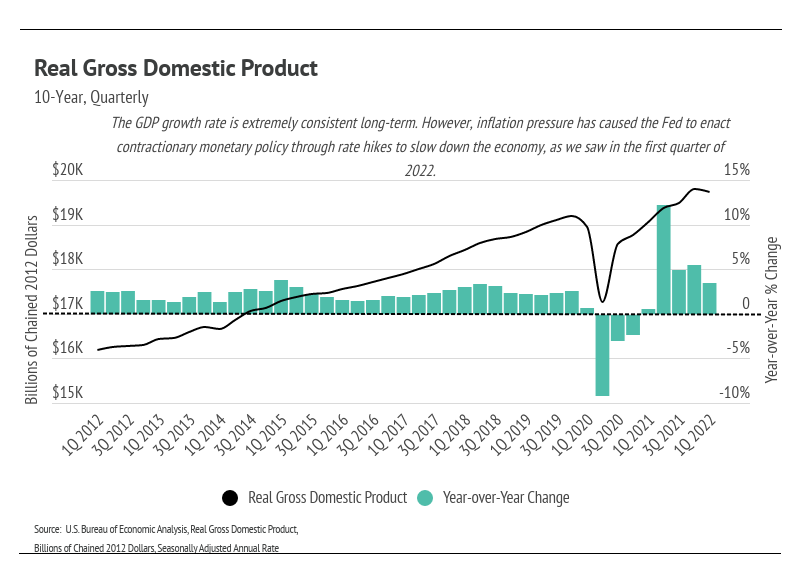

But what about the Fed’s intention to slow down the economy by decreasing demand through raising rates? Won’t that cause a recession and lower home prices? We’ve already seen some slowdown in the Q1 2022 Real Gross Domestic Product (GDP)* data. The Fed’s goal is to slacken growth enough to curb inflation, but not enough to send the U.S. into a recession, which is a challenging needle to thread. The National Bureau of Economic Research, which officially declares recessions, defines a recession as a significant decline in economic activity spread across the economy that lasts more than a few months and is normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. With unemployment near all-time lows and a surplus of job openings, we may end up avoiding an official recession, even if GDP decelerates for multiple quarters. U.S. GDP is expected to outpace China’s this year for the first time since 1976, which sounds positive but could be a clear sign of a major slowdown given our economic ties.

Home prices are highly likely to continue rising despite rising rates. If you were waiting for rates to drop, they won’t. The low but rising supply continues to make the market competitive and, as more homes come to market, could mark the early stages of market normalization. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

*Real GDP is inflation-adjusted GDP, which is the broadest measure of goods and services produced. All references to GDP use Real GDP figures.

Big Story Data

The Local Lowdown

Quick Take:

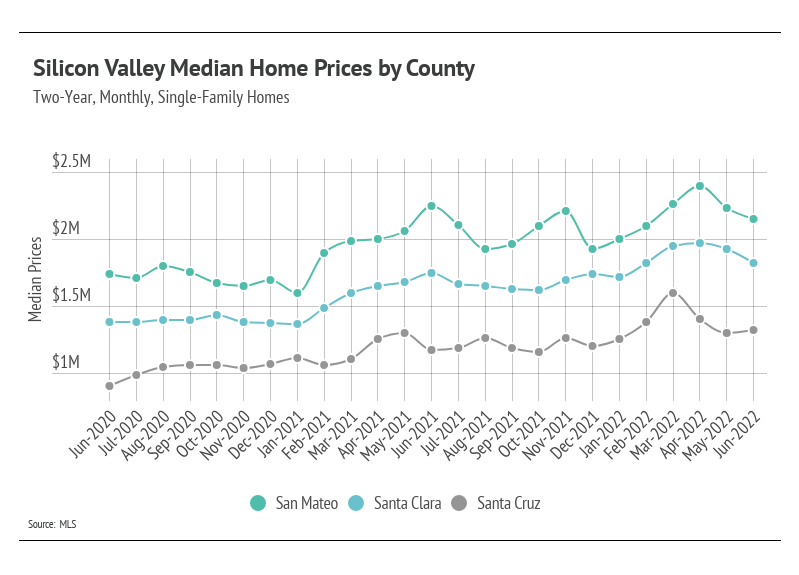

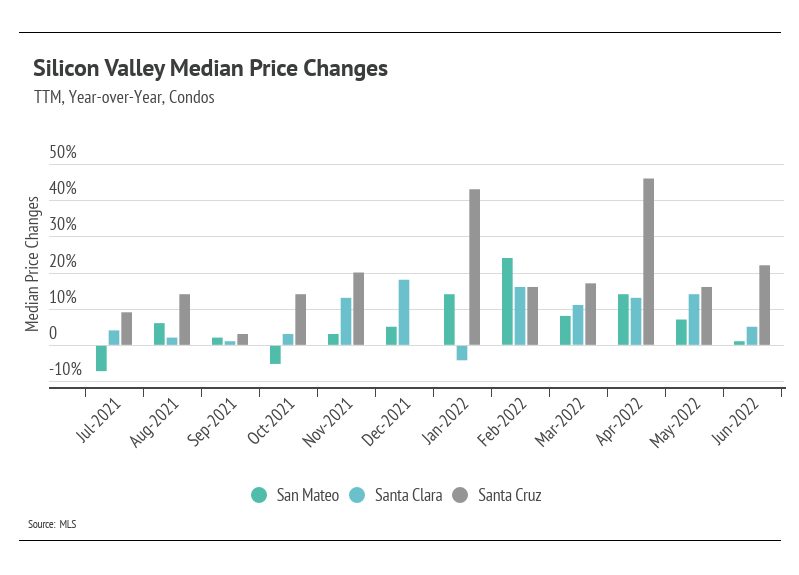

Home prices in Silicon Valley may be hitting a soft ceiling after two years of rapid price increases.

2022 began with huge demand in the first quarter, but that demand has slowly dwindled throughout the year. Housing inventory will likely follow the normal seasonal trends; however, the new normal will include historically low inventory.

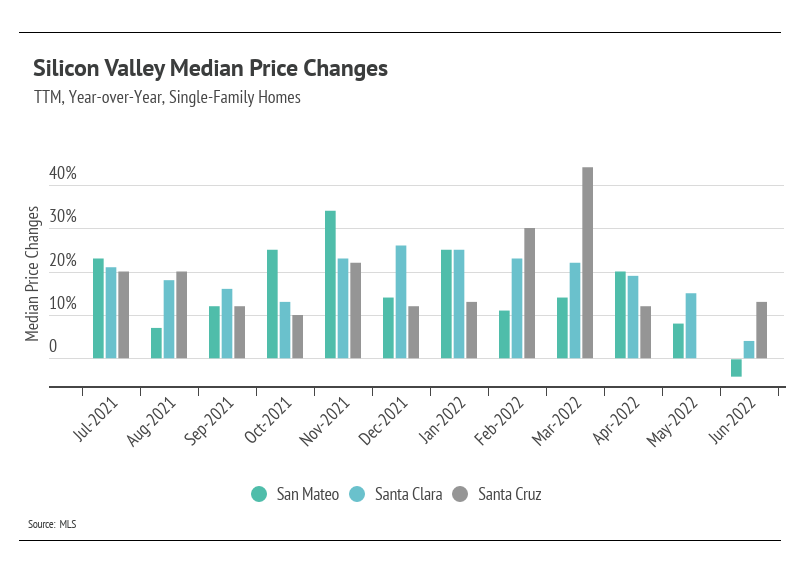

Home price appreciation is moving toward a more sustainable growth rate: around 6–8% annually.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

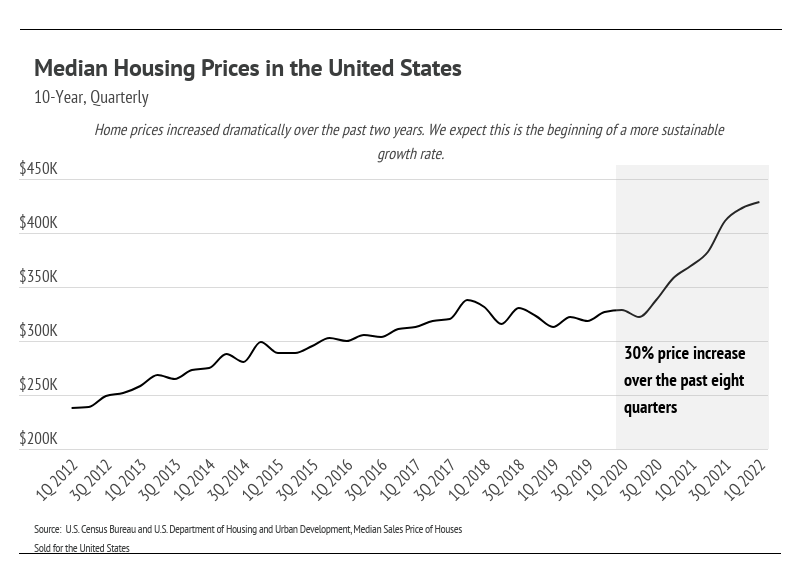

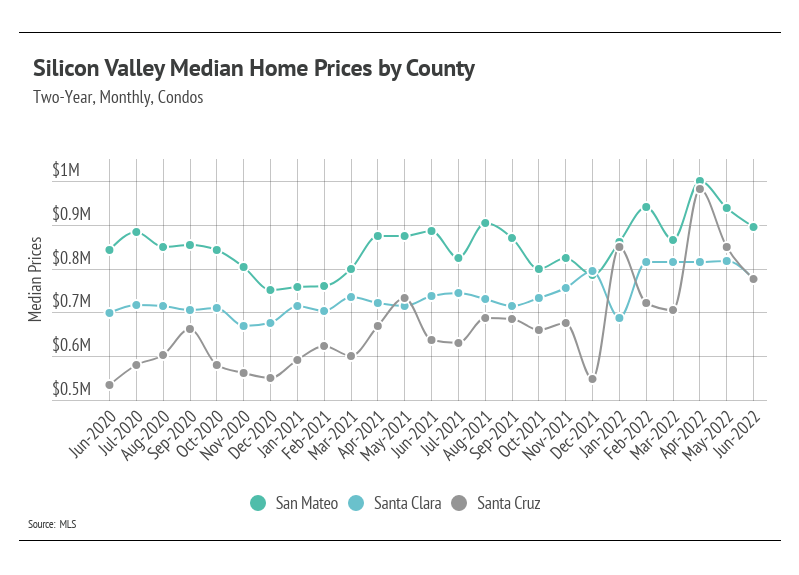

Home prices soften in May and June

The median single-family home and condo prices in Silicon Valley continued to decline from their April peaks, but they’re still historically high. After two years of significant price growth across markets and dwelling types, it’s hard not to think that rate increases have caused prices to creep near a ceiling. Without the aid of super low financing options, fewer potential buyers will participate in the market. So far in 2022, the average 30-year mortgage rate has increased over 2.5%, which equates to an approximately 33% increase in monthly mortgage payments. In other words, the new mortgage rate adds $730 per month on a $500,000 30-year fixed mortgage, for example (double that for a $1 million loan).

Even with the rate hikes, which are only expected to continue this year, home prices aren’t dropping outside of normal month-to-month variability, nor would we expect them to. Supply is still historically low, which will protect prices from experiencing a major downturn. Prices will likely follow a similar trend to last year, with mild growth through the summer and fall months. But, as we mentioned earlier, as rates increase, the same price becomes more expensive, unless you are buying with cash.

It’s so incredibly easy to get wrapped up in the recent past, during which home prices grew quickly. We can’t stress enough how uncommon that price growth was and, most likely, will continue to be. Because homes are not only living spaces but also investments, a steadier growth rate of 6–8% annually is still good for investing purposes.

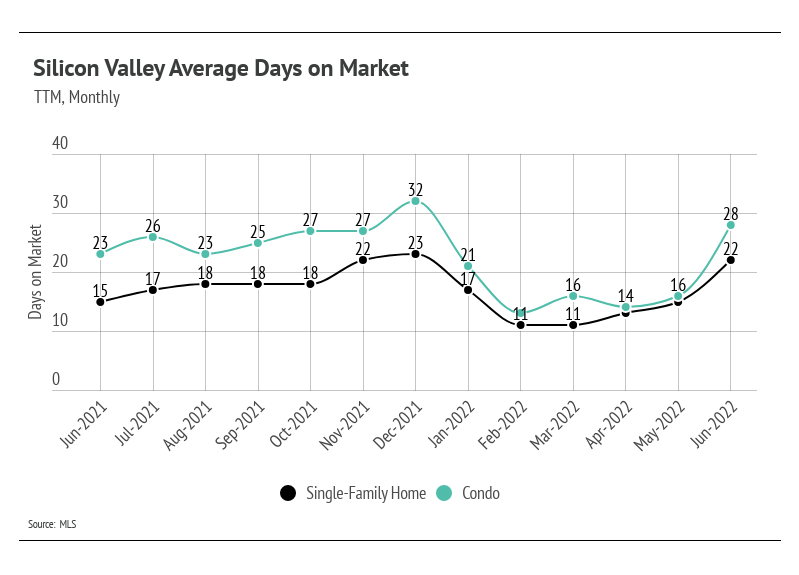

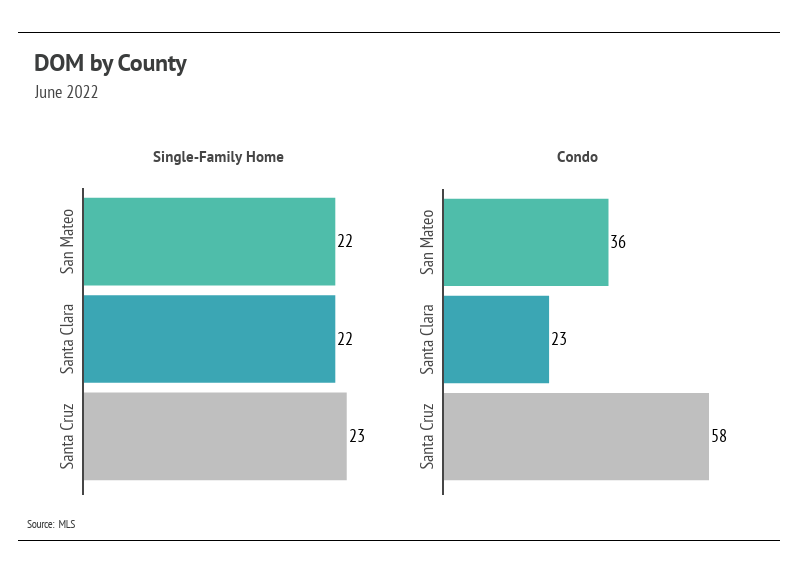

Sales slowdown

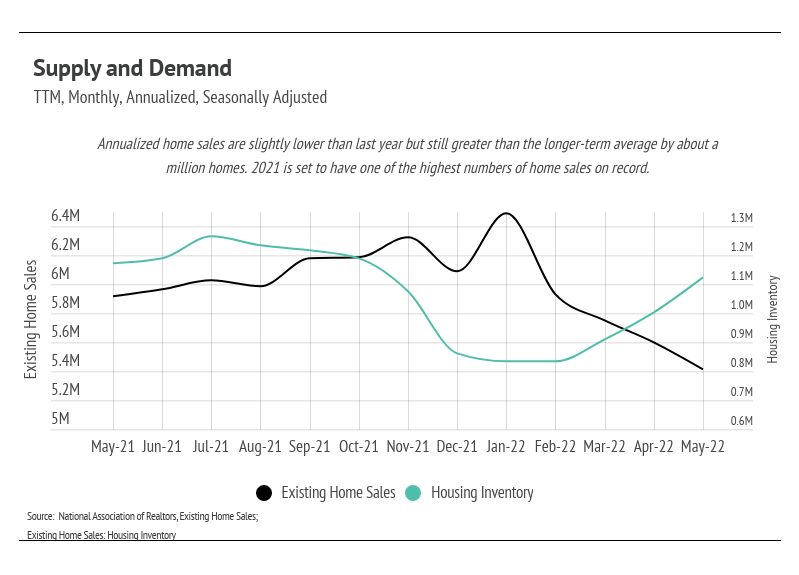

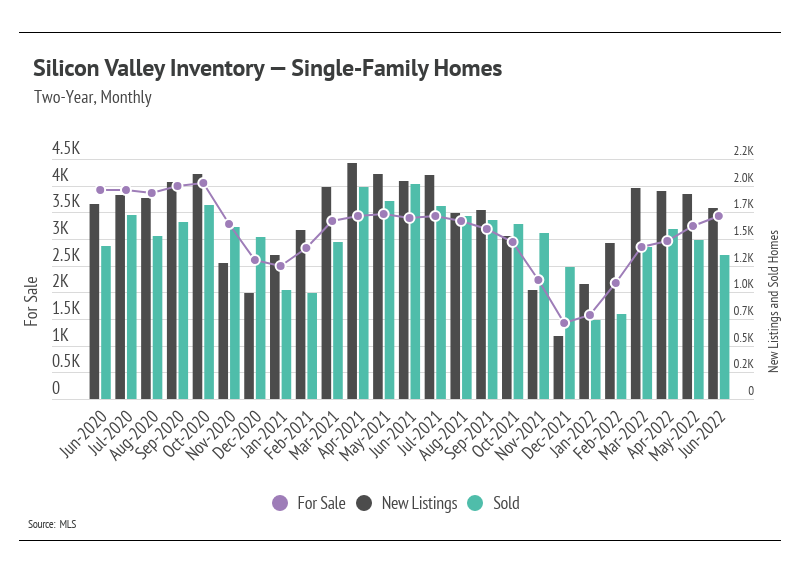

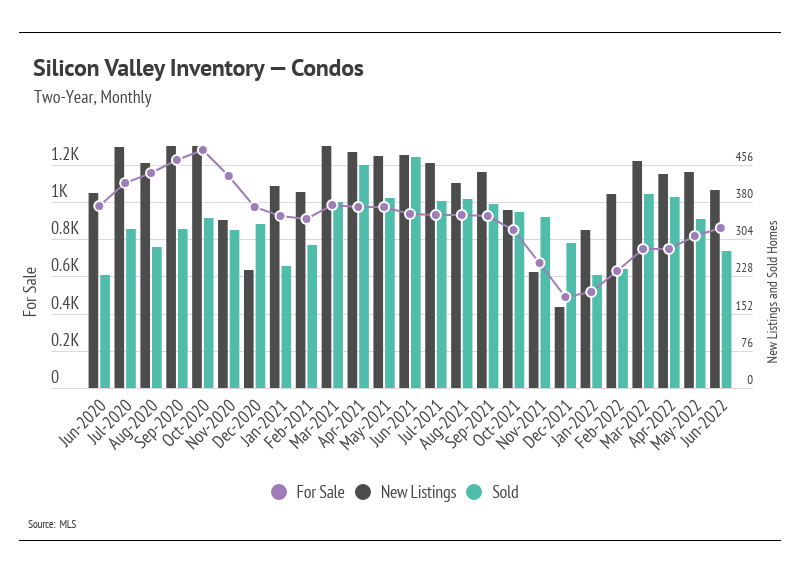

Silicon Valley’s housing inventory continued to rise in June, following historical seasonal trends. Since March 2020, inventory has trended lower and settled at a depressed level. The number of single-family homes and condos on the market in June 2022 is 12% lower than in June 2020. Although the first half of 2022 had one of the lowest inventories on record, we were pleased to see that inventory increased, a trend that usually holds until mid-summer. With June inventory continuing to rise, the next two to three months will likely show us peak inventory levels for 2022, which will undoubtedly be the lowest peak inventory on record.

In June, sales declined along with new listings, potentially indicating that demand is softening. This isn’t to say demand is low, however, especially relative to supply. Sellers can expect multiple offers, and buyers should come with competitive offers.

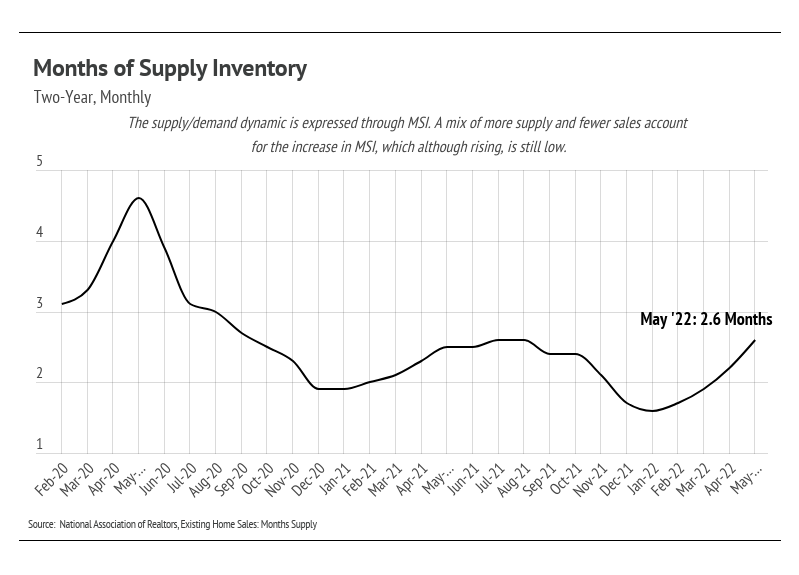

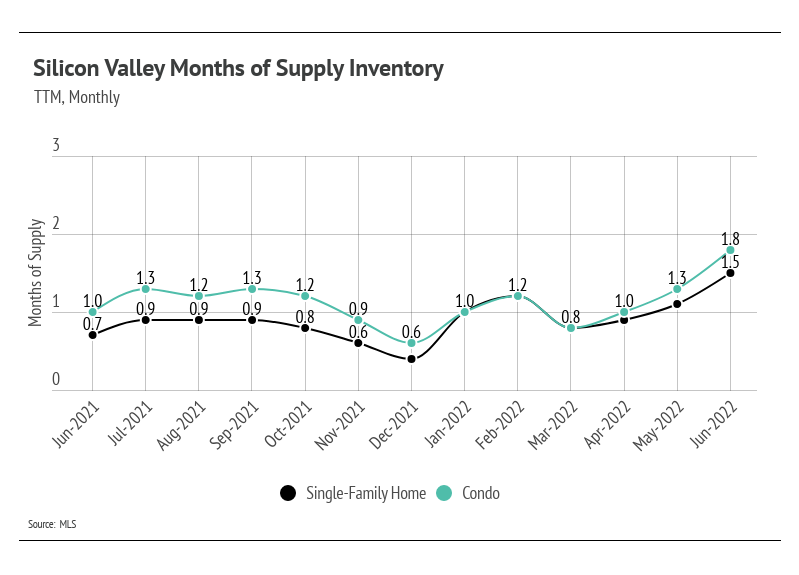

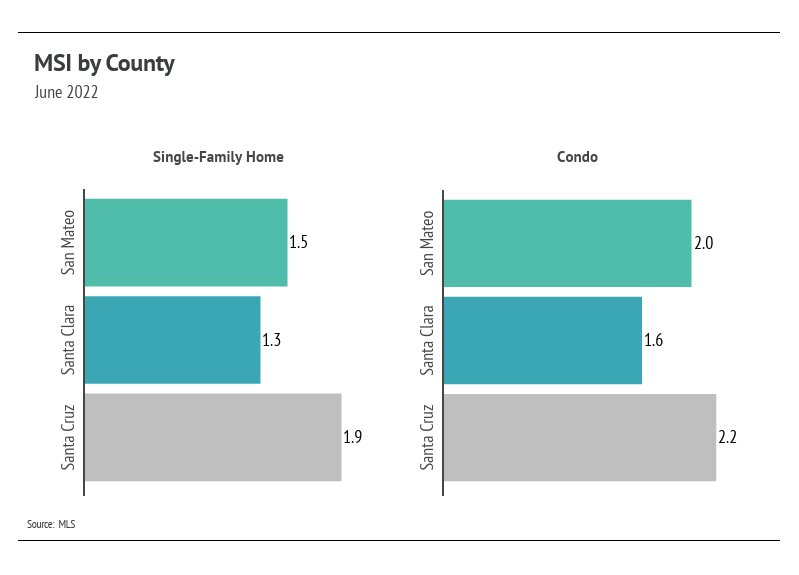

Months of Supply Inventory increasing, but still a sellers’ market

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). Although MSI has risen over the last three months, single-family home and condo MSIs are still low, indicating a sellers’ market.