San Francisco Real Estate Market Report: February 2021

michelle February 1, 2021

michelle February 1, 2021

Welcome to our February newsletter. This month, we cover the state of employment in the United States and the likelihood of meaningful stimulus. We also dive into how the Democratic Party’s majority control over both chambers of Congress and the White House could affect asset prices and interest rates.

Most of California (around 98% by population) is under a stay-at-home order due to COVID-19, and the United States as a whole is seeing new peaks every day. With the approval of several vaccines, we finally have a glimmer of hope to move out of the pandemic. However, we know that transmission mitigation measures will still be necessary through 2021 at least. The pandemic has substantially raised demand for housing, and we suspect that demand will continue through this year. Mortgage rates remain at all-time lows, and buyers are devoting more of their total spending to housing costs.

As we enter the new year, we continue to provide you with the most up-to-date market information so that you feel supported and informed in your buying and selling decisions.

In this month’s newsletter, we cover the following:

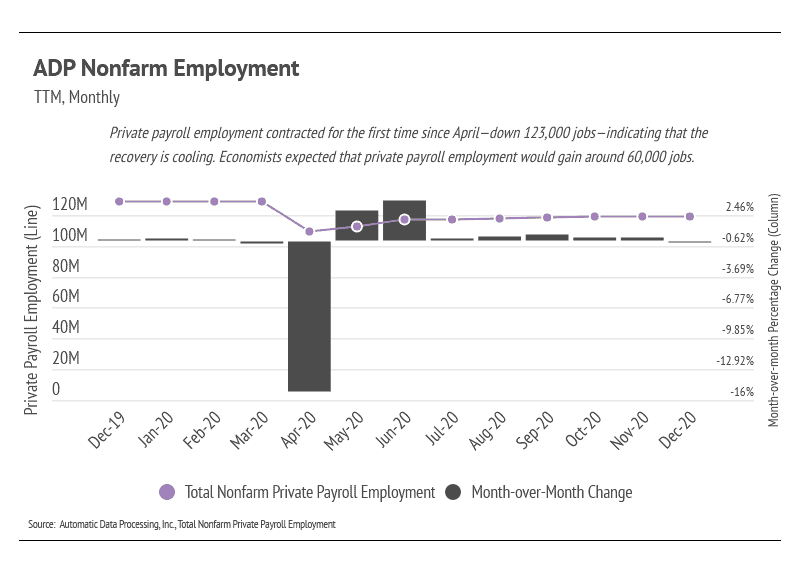

According to the ADP private payrolls, the U.S. lost 123,000 jobs in December 2020, marking the first contraction since April. Economists predicted an increase of around 60,000 jobs in December. However, they did not anticipate larger companies, especially in leisure and hospitality, laying off employees due to reimplementation of stricter COVID-19 restrictions.

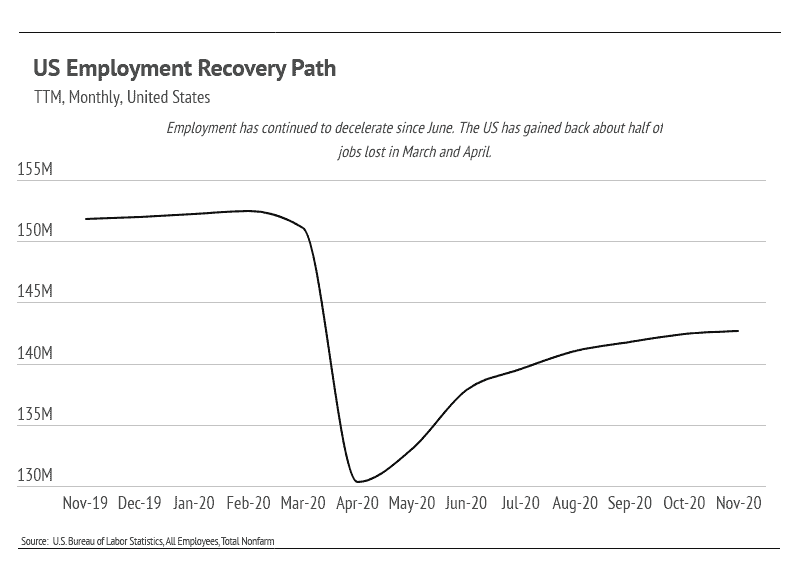

Data from the Bureau of Labor Statistics differs in the exact numbers but shows the obvious deceleration in employment growth. As time passes, more and more jobs will be permanently lost, likely with real long-term economic impact: fewer people interacting in the economy usually indicates less buying, which trickles into less production, which trickles into fewer workers needed, leading to more unemployed workers.

Job growth is one of the clearest indicators of economic health, so the December jobs contraction underscores a slowing of the recovery and the need for government stimulus. Under the incoming presidential administration, government stimulus is far more likely but will take some time to implement. With aid, businesses will be able to continue operating and will likely be able to hire significant numbers of employees back, setting the recovery back on course.

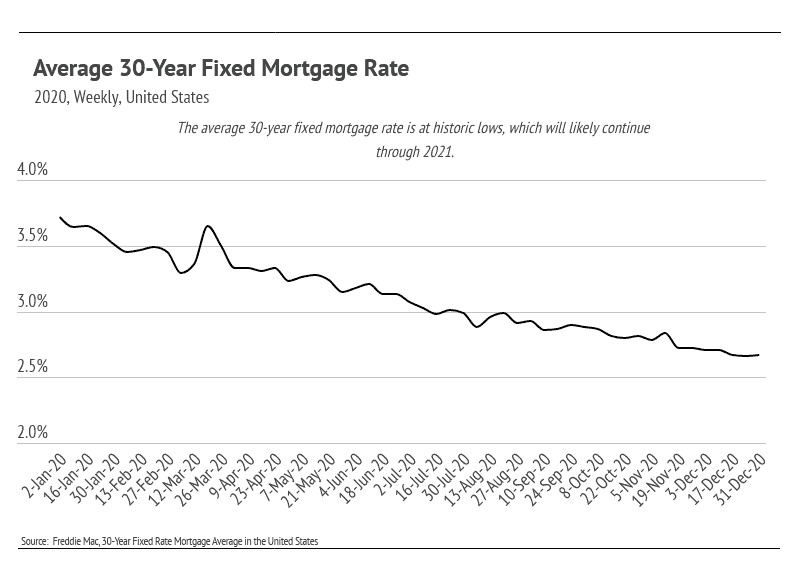

To help struggling businesses and people, the government will have to spend significant amounts of money. Heavy fiscal spending is often associated with higher inflation. Currently, inflation is around 1.2% (the Federal Reserve targets 2%), and with the expected increase in government spending, the expected inflation will rise as well. Ultimately, money today is worth more than money in the future. Not only can you buy more today, but real interest rates (inflation-adjusted interest rates) will be lower as well, making a home bought today cost less than its future price.

For example, the average 30-year mortgage rate is 2.67%, and if the inflation rate were 2%, the real interest rate on the mortgage would be 0.67%.

The financial circumstances on the individual level are highly variable, now more than ever. Those who have been unaffected (or even positively affected) financially are likely saving more money than ever. Strict COVID-19 restrictions have largely cut travel, dining, and entertainment expenses, allowing potential home owners to devote more of their income toward buying a home that they love. With historically low mortgage rates and an expected increase in inflation, it’s never been cheaper to finance a home.

Demand shows no sign of decline in the near term. Today, housing is one of the best investments one can make, as it has been historically.

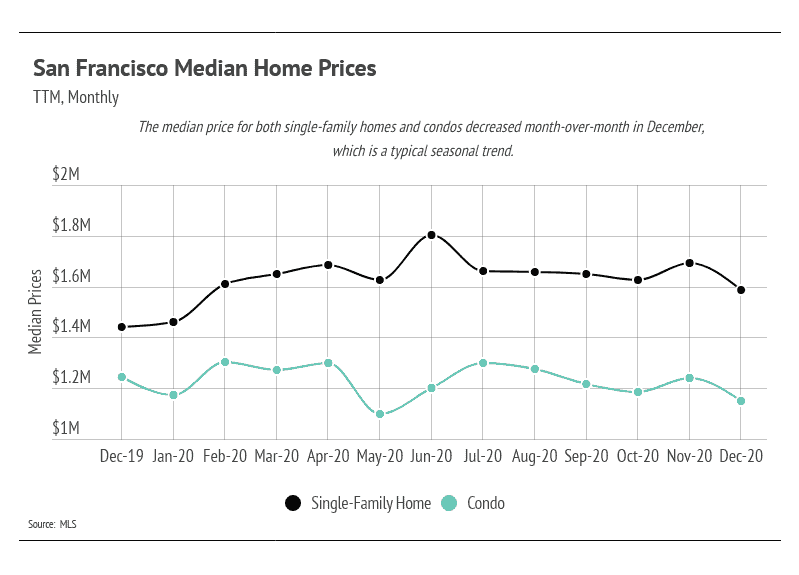

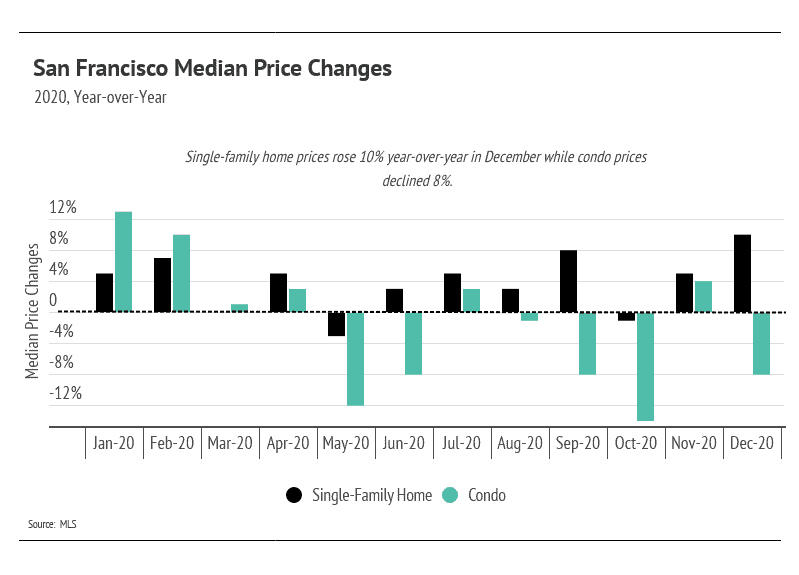

The median single-family home and condo prices fell month-over-month, which is typical for the winter season. Year-over-year, single-family home prices increased considerably, up 10%, while condos were down 8%. Inventory has continued to decline as fewer homes have come to market and sales have remained high. Inventory for condos is almost twice as high relative to last year, which has been the primary driver of price decreases.

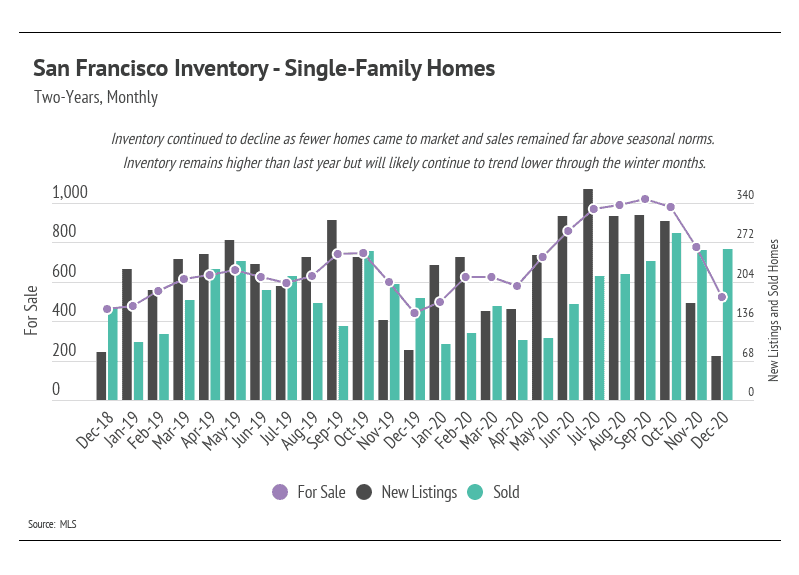

Single-family home sales have climbed since the initial months of the pandemic (March through May). Generally, buyers and sellers left the market in April and May, causing pent-up demand. Since May, sales have increased and were still near their highest levels in 2020 for single-family homes. Usually, we expect sales to decline in the autumn and winter months, but the 2020 summer selling season was delayed and seems to be spilling well into the autumn/winter season. Single-family home inventory dropped precipitously over the last two months due to unusually high sales numbers, and it is likely to decline further as we make our way through the winter months.

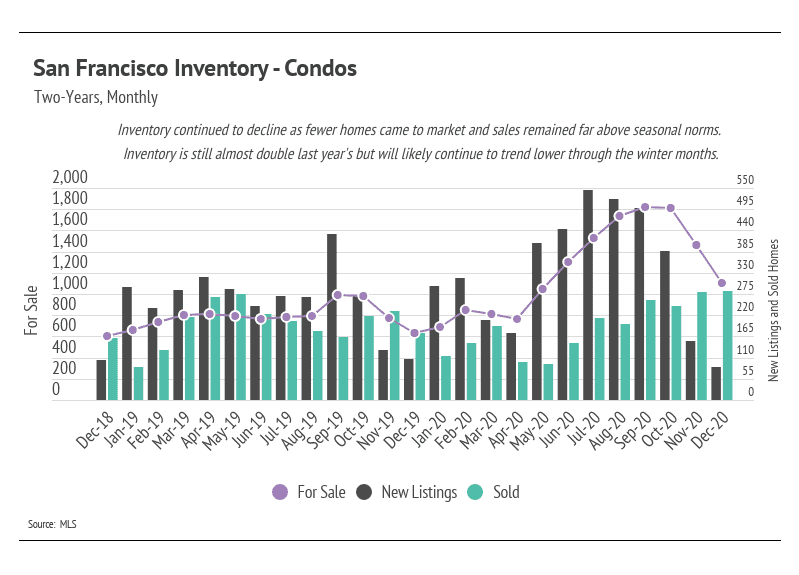

The number of condos on the market declined significantly in December. New condos coming to market outpaced sales every month in 2020 except for November and December, when sales were far greater than new supply. In December, condo inventory was still 75% higher than it was last year, but we are pleased to see a reduction in some of the excess inventory.

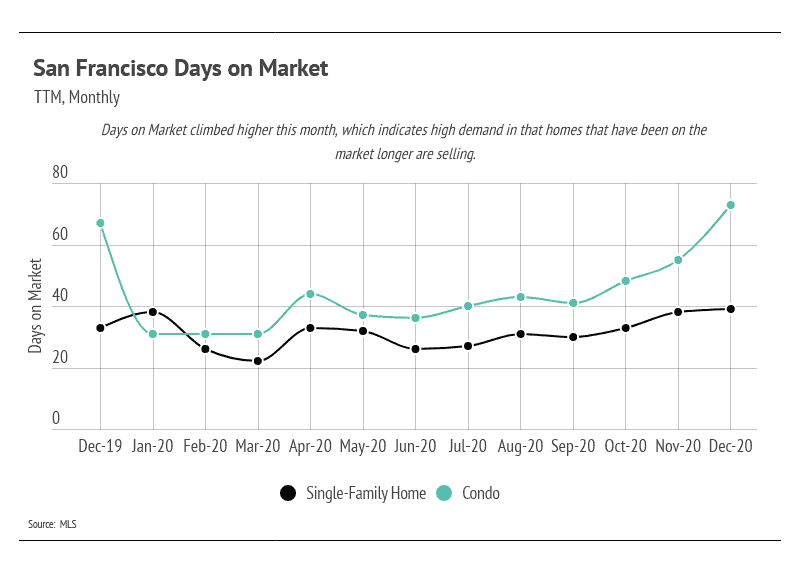

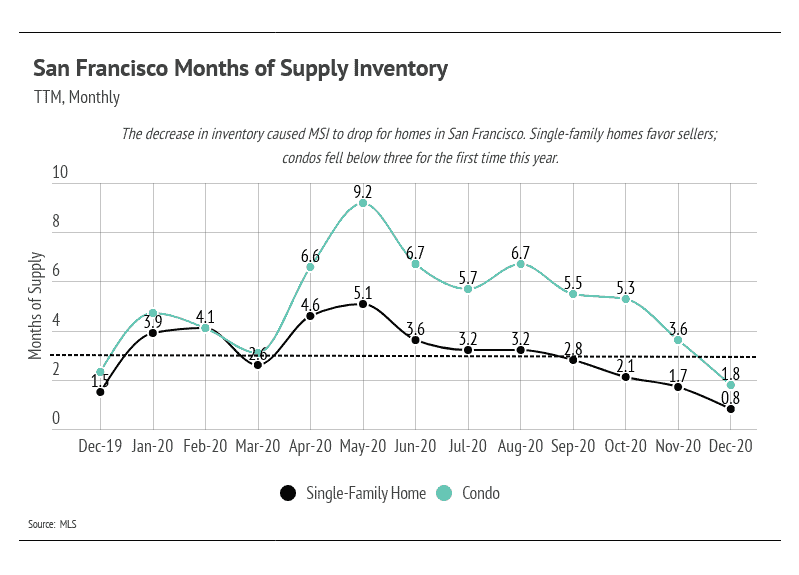

Days on Market (DOM) was higher in December, which is attributed to sold homes that have been on the market for longer than average. Normally, rising DOM indicates a slowing market, but that is not the case for San Francisco. Inventory built to a level that demand could not meet, so homes stayed on the market longer than usual. As we will see, the pace of sales affects Months of Supply Inventory (MSI) and has contributed to the low MSI over the past several months.

We can use MSI as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California (far lower than the national average of six months of supply), which indicates a balanced market. An MSI lower than three means that buyers dominate the market and there are relatively few sellers (i.e., it is a sellers’ market), while a higher MSI means there are more sellers than buyers (i.e., it is a buyers’ market). The MSI dropped below one for single-family homes, which firmly favors sellers. The MSI for condos fell considerably and now indicates a sellers’ market; however, we view the condo market to be more balanced considering the current inventory level.

In summary, the high demand in San Francisco has sustained home prices. Inventory for single-family homes and condos will likely decline further into the new year, and fewer sellers will likely come to market, potentially lifting prices higher. The condo market is still experiencing an oversupply, but is trending lower. Overall, the housing market has shown its resilience through the pandemic and remains one of the safest asset classes. The data show that housing has remained consistently strong through this period.

The autumn/winter season tends to see a slowdown in activity, although we may see a new trend this year with higher-than-normal sales.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

Stay up to date on the latest real estate trends.

Michelle Kim | July 17, 2026

Discover the strategies that help San Francisco homes stand out, attract serious buyers, and maximize value before they even hit the market.

Michelle Kim | July 10, 2026

Avoid the most common mistakes homeowners make before listing their property and learn how preparation, pricing, and marketing can help you achieve a successful home s… Read more

Michelle Kim | July 6, 2026

Learn the key factors that help San Francisco homes attract multiple offers, from strategic pricing and professional marketing to home presentation and buyer demand.

Michelle Kim | July 1, 2026

Quick Take: Prices are rising across much of the Bay Area, with San Francisco single-family homes breaching the $2.2 million mark for the first time and the East Bay p… Read more

Michelle Kim | July 1, 2026

Quick Take: Median sale prices posted gains in three of four counties, with Sonoma County leading the way at 2.33% year-over-year growth, while Marin County saw a 4.70… Read more

Michelle Kim | July 1, 2026

Quick Take: Prices are on the rise across the board, with single-family homes and condos both posting year-over-year gains for the first time in over a year. Inventory… Read more

You’ve got questions and we can’t wait to answer them.