Greater Bay Area Real Estate Market Report: June 2022

saudra June 1, 2022

saudra June 1, 2022

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

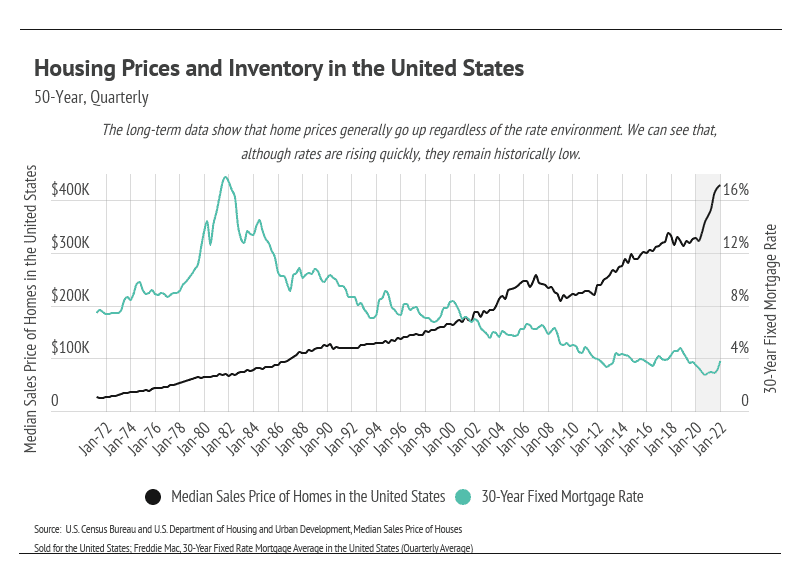

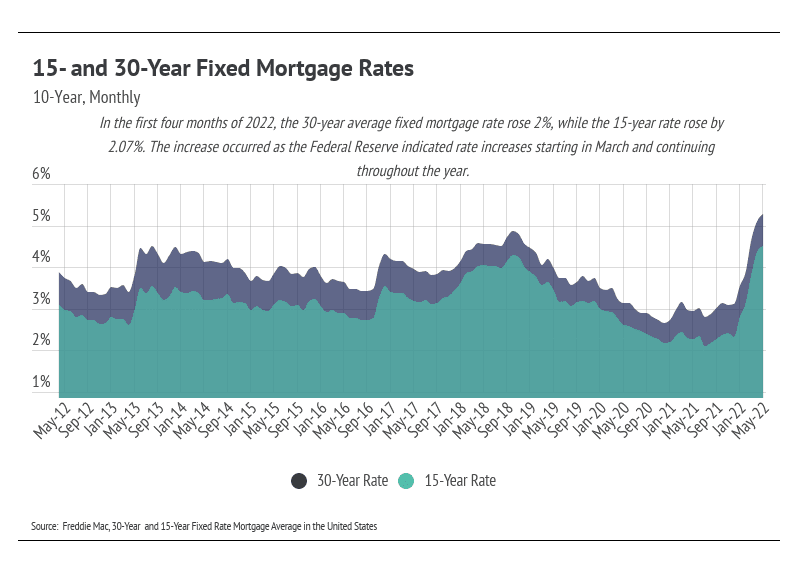

After the Fed’s May meeting, Fed Chair Jerome Powell announced that they are raising their benchmark rate by 0.50%, the largest hike since 2000. Earlier this year, the Fed was expected to raise interest rates by 0.25% at least six times this year, going from 0% to 1.90%. Now that each increase will most likely be 0.50%, the market expects the federal funds rate to reach 2.75% to 3.00% by the end of the year, which would be the highest in 15 years. Although the fed funds rate doesn’t directly affect mortgage rates, the rate hike moves into the broader economy quickly. Over the past four months, mortgage rates have moved about 2% higher for both 30- and 15-year fixed mortgages. Economists now estimate that 30-year mortgage rates could climb above 6% by mid-2022, which is fast approaching. Because the Fed indicated the path of rate hikes for the rest of the year, we expect mortgage rates to top out at around 7% this year for prime borrowers.

A rising rate environment increases short-term demand as buyers try to lock in lower mortgage rates, which is what we are seeing now. The increased short-term demand is driving prices right now outside of supply, which begs the question: Will higher mortgage rates actually drive down prices? No, they sure won’t.

Using history as our guide, we can see that home prices continued to rise even as mortgage rates peaked at over 18% in the 1970s, which would translate to about $7,500 per month on a $500,000 loan. Luckily, we aren’t going back to those rates. Higher rates, however, will do exactly what the Fed intends, which is to take money out of the economy and decrease overall demand. The average 30-year mortgage rate was 3.11% in December 2021, rising to 5.10% by the end of April 2022. If you bought a home in December and financed it with a $500,000 mortgage loan at 3.11%, your monthly spend on principal and interest would be $2,138 — versus $2,715 if you got the same loan in April 2022 at 5.10%. Over the life of the loan, you’ll spend $207,720 more at 5.10%. From the Fed’s perspective, that equates to roughly $500 less per month to spend on goods and services, bringing down aggregate demand when we multiply that reduction of disposable income across households. The gradual rate increases are meant to avoid sending the economy into a recession.

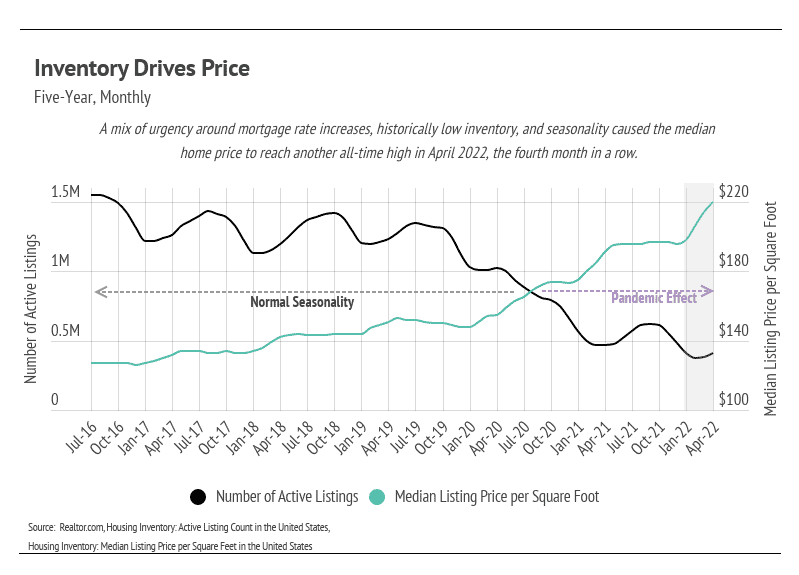

In addition to rising rates, supply still drives home prices. In April, the housing supply ticked up ever so slightly, but it’s still 60% lower than the number of homes on the market in April 2020. We are entering what is traditionally the hottest time of year for the housing market with a record low supply of homes. Over the past four months, which had the lowest inventory on record, home prices increased 12%.

If you are considering buying a home, there aren’t many reasons to wait. Home prices and rates are still rising. The low supply continues to make the market extremely competitive. We are starting to see some softening in demand, but not nearly enough to balance the supply side of the market.

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

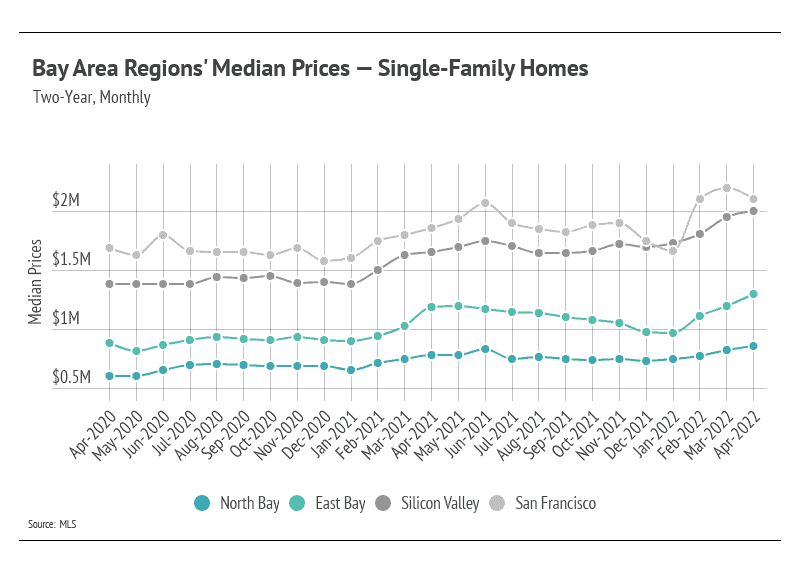

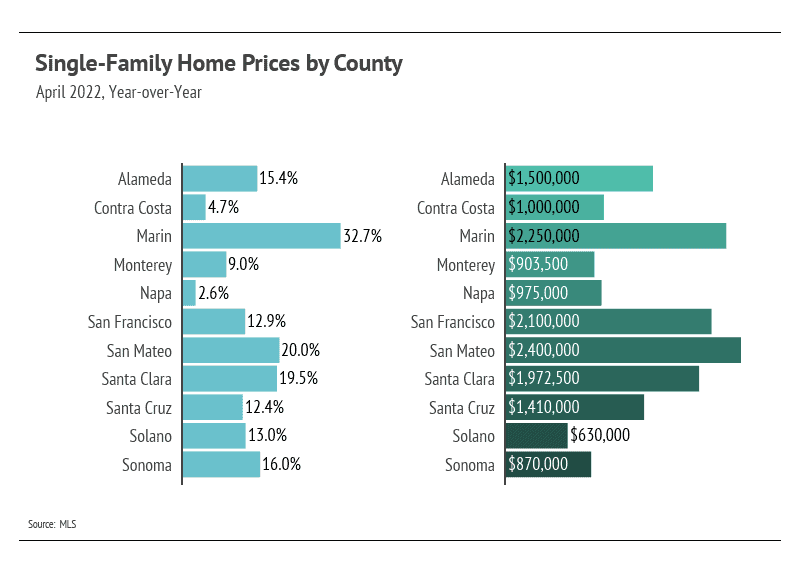

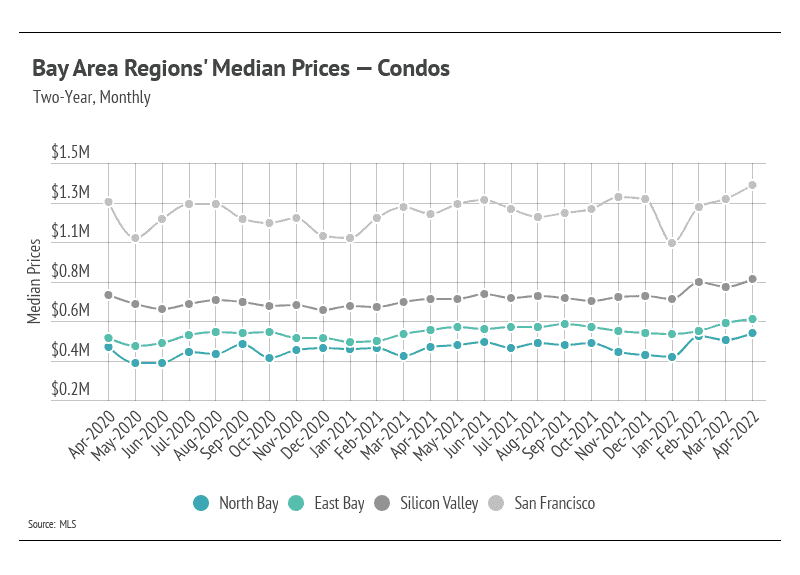

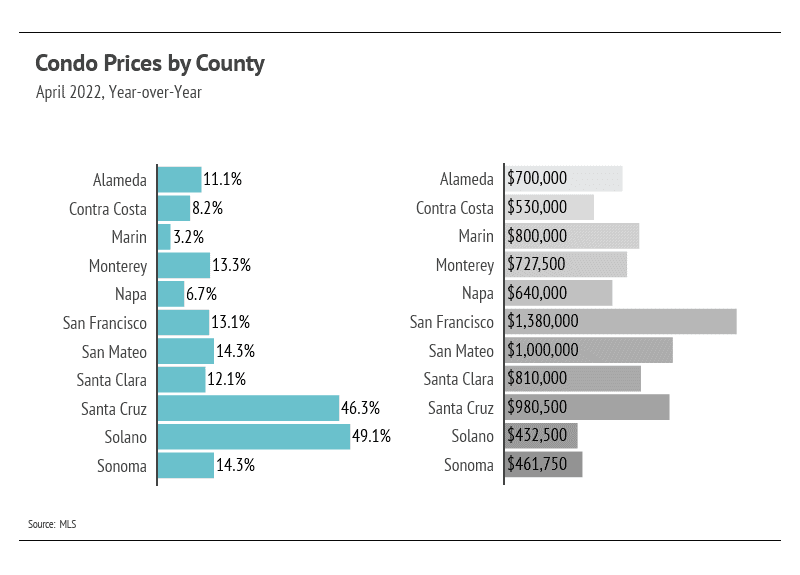

Single-family home and condo prices rose to all-time highs in April 2022 across much of the Greater Bay Area, but it’s still too early to determine how increasing rates will affect the market. Mortgage rate hikes only lower demand in the long term. In the short term, demand increases as buyers try to lock in lower rates. Over the past four months, the average 30-year mortgage rate has increased 2%, which means a 27% increase in monthly mortgage payments, yet prices keep moving higher.

The factors now affecting home prices are anticipated to have mixed results, unlike the past two years when all factors caused prices to increase. Rising interest rates, which will hopefully curb the rising 40-year-high inflation rate, will make homes less affordable and dampen demand over the rest of the year. They may, however, also lower supply as current homeowners reconsider their plans to sell.

Many homebuyers are also home sellers, moving from one home to another. Newer homebuyers and homeowners who refinanced over the past two years locked in one of the lowest rates in history, making moving a more difficult financial decision. This could keep supply unseasonably low with fewer new listings coming to market, as we saw in April. In general, the Fed doesn’t have a tool to deal with supply-side issues: It uses monetary policy to affect demand, making money more or less expensive. As a result, the Fed’s rate hikes may result in unintentional effects on supply. In the Bay, the lack of housing supply will keep prices rising in the coming months.

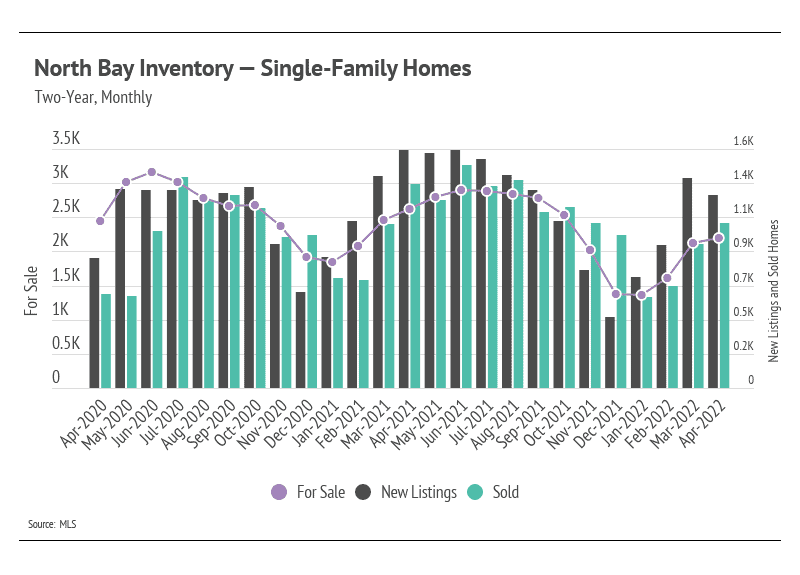

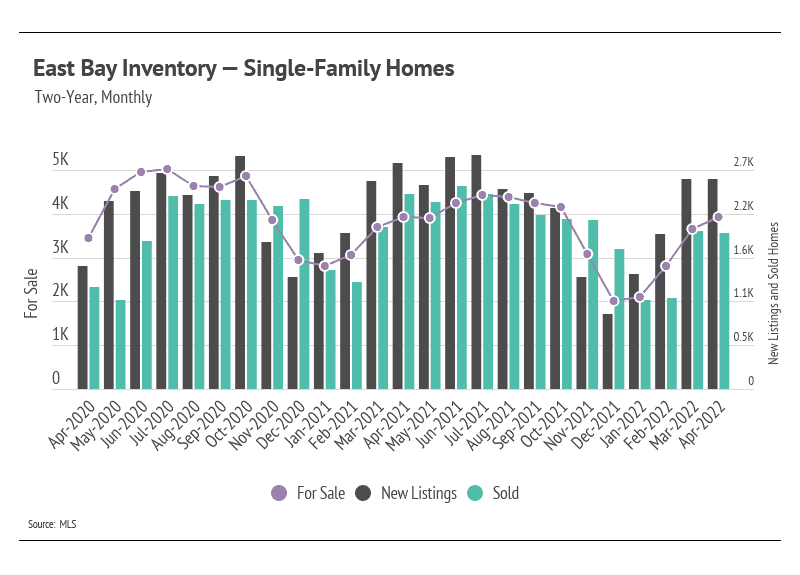

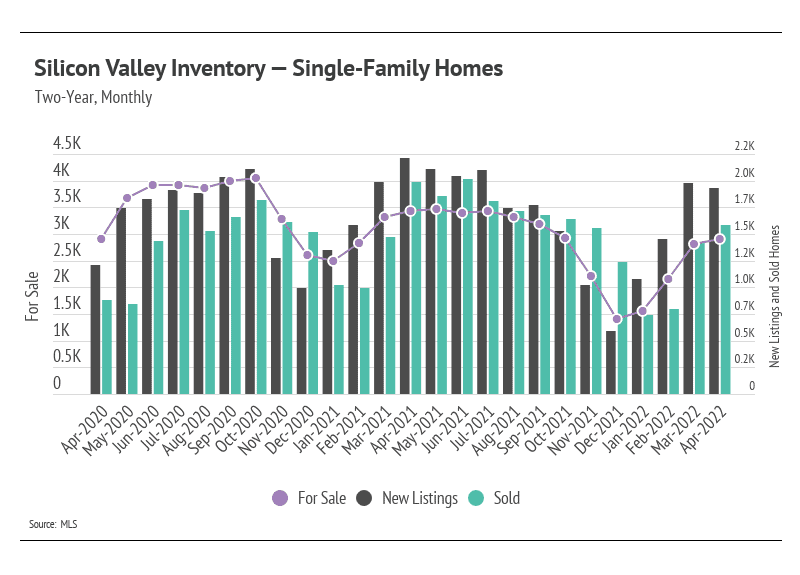

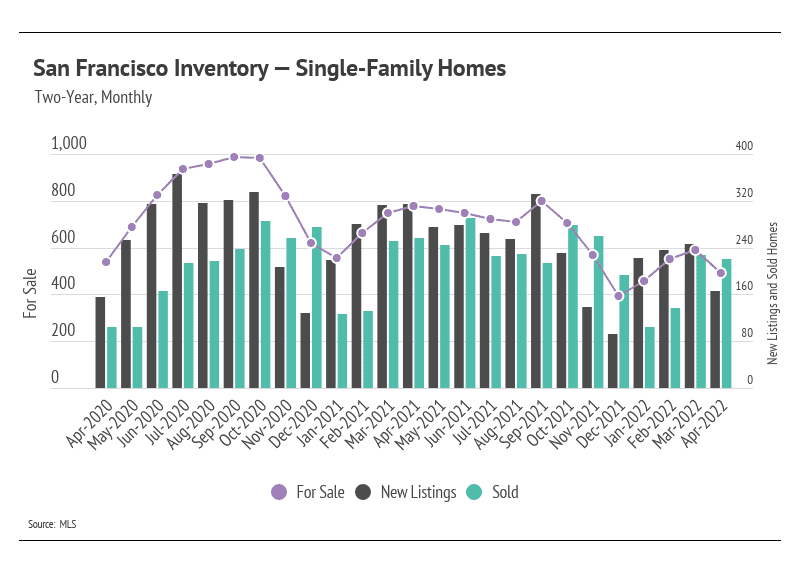

In the Greater Bay Area, inventory continued to climb in April, which is great news for the highly undersupplied market. However, new listings declined from March to April, far from the seasonal norm and an early indicator that home supply will remain depressed this year. The high demand and lack of new listings over the past year brought single-family home and condo supplies to record lows across markets as we entered 2022. We were pleased to see that inventory increased over the first four months of the year, a trend that usually holds until mid-summer. The next three months will be telling of how inventory levels will trend for the rest of the year.

Even though inventory is low, sales remain incredibly high, especially when we account for available supply. This trend once again highlights the high demand in the area. Sellers can expect multiple offers, and buyers should come with competitive offers.

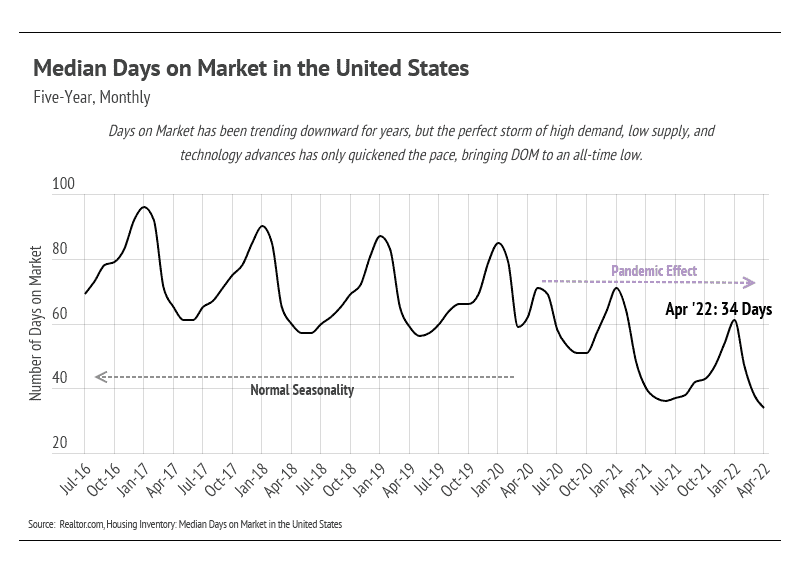

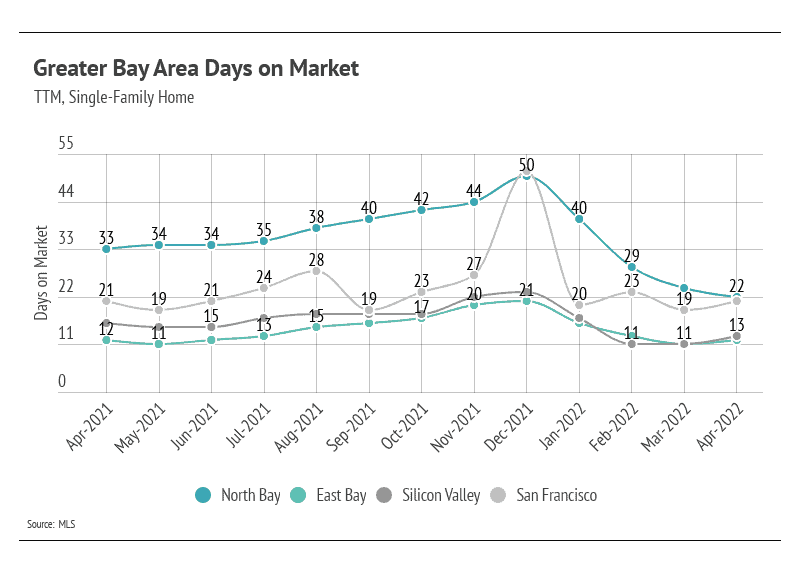

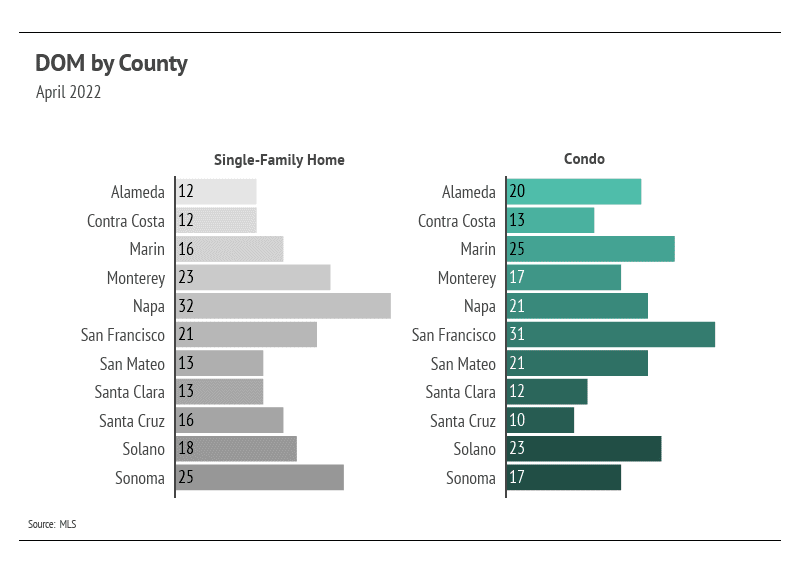

Homes are still selling extremely quickly. The Days on Market reflects the high demand for homes in the Greater Bay Area. Buyers must put in competitive offers above the list price of the home.

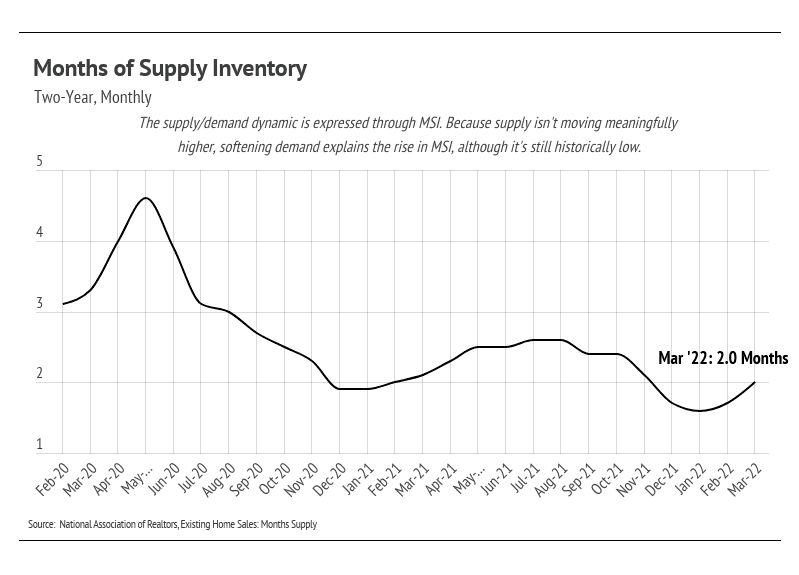

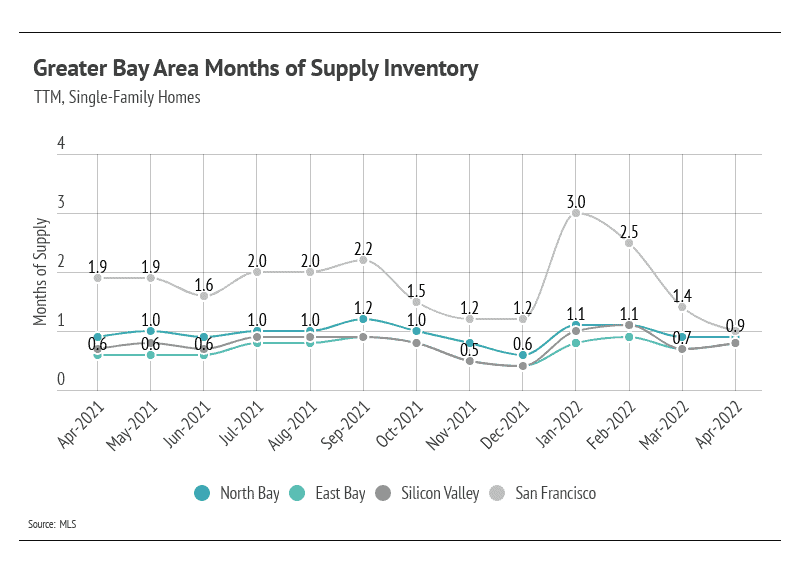

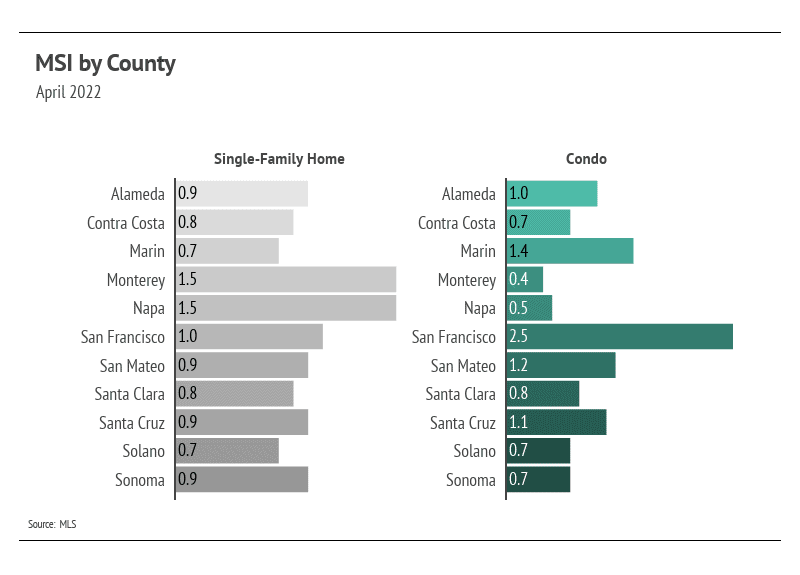

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). Currently, single-family home and condo MSIs are exceptionally low, indicating a strong sellers’ market.

Stay up to date on the latest real estate trends.

Michelle Kim | July 17, 2026

Discover the strategies that help San Francisco homes stand out, attract serious buyers, and maximize value before they even hit the market.

Michelle Kim | July 10, 2026

Avoid the most common mistakes homeowners make before listing their property and learn how preparation, pricing, and marketing can help you achieve a successful home s… Read more

Michelle Kim | July 6, 2026

Learn the key factors that help San Francisco homes attract multiple offers, from strategic pricing and professional marketing to home presentation and buyer demand.

Michelle Kim | July 1, 2026

Quick Take: Prices are rising across much of the Bay Area, with San Francisco single-family homes breaching the $2.2 million mark for the first time and the East Bay p… Read more

Michelle Kim | July 1, 2026

Quick Take: Median sale prices posted gains in three of four counties, with Sonoma County leading the way at 2.33% year-over-year growth, while Marin County saw a 4.70… Read more

Michelle Kim | July 1, 2026

Quick Take: Prices are on the rise across the board, with single-family homes and condos both posting year-over-year gains for the first time in over a year. Inventory… Read more

You’ve got questions and we can’t wait to answer them.