East Bay Real Estate Market Report: April 2021

michelle April 7, 2021

michelle April 7, 2021

Welcome to our April newsletter. This month, we examine how housing affordability in California may affect future demand by looking at housing affordability in relation to price, interest rates, and per capita income.

COVID-19 cases continue to decrease after peaking in January. The United States is administering nearly two million vaccinations a day, and projects it will be able to vaccinate all U.S. adults by the end of May. While the feeling of hope is palpable, COVID-19 will continue to affect how we live and work for quite some time. We expect demand for housing to remain high for years to come. Even as it becomes safer for people to interact in office settings, we anticipate that working remotely, even if not every day, is here to stay. With less uncertainty around the future, the period of all-time-low mortgage rates is coming to a close, which may boost demand even further over the next several months.

As we navigate an ever-changing economic landscape, we remain committed to providing you with the most up-to-date market information so you feel supported and informed in your buying and selling decisions.

In this month’s newsletter, we cover the following:

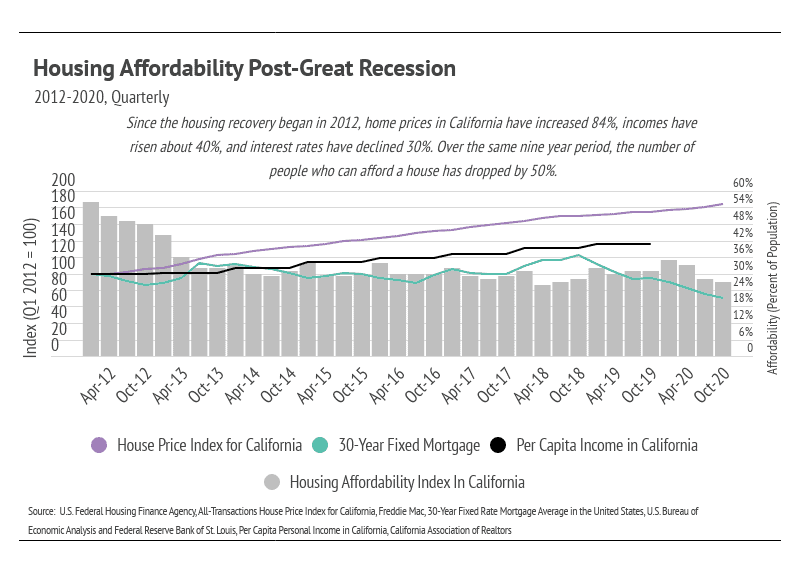

Important trends to discuss this month are the connection between housing affordability and housing demand in California and the effects of rising mortgage rates. The chart on the next page compares the indices of three metrics—home price in California, the average 30-year mortgage rate in the United States, and per capita income in California—against housing affordability in California.

After the 2008 financial crisis, housing didn’t truly begin to recover until January 2012. As we can see from the chart, housing was most affordable in the first quarter of 2012 with 56% of the population estimated to have the means to afford a home. Within two years, affordability declined to a more steady state of around 30%. During the nine-year period that the chart depicts (Q1 2012–Q4 2020), homes in California, on average, increased in price over 80%. Of those homes, those in major metropolitan areas saw greater price appreciation. During the same period, per capita income increased around 40%, and mortgage rates moved between slightly under 3% to 5%, with an average of 3.87%.

Interest rates have an interesting effect on affordability, but income level, unsurprisingly, seems to have the most influence. According to the California Association of Realtors (CAR), the minimum qualifying annual income has increased 129% for single-family homes and 111% for condos since the first quarter of 2012. If we compare 129% minimum income increase to the 40% per capita income increase during that same time, we clearly see why homes have become broadly less affordable. Currently, 27% of Californians can afford a home, and that number will likely decrease over the next year.

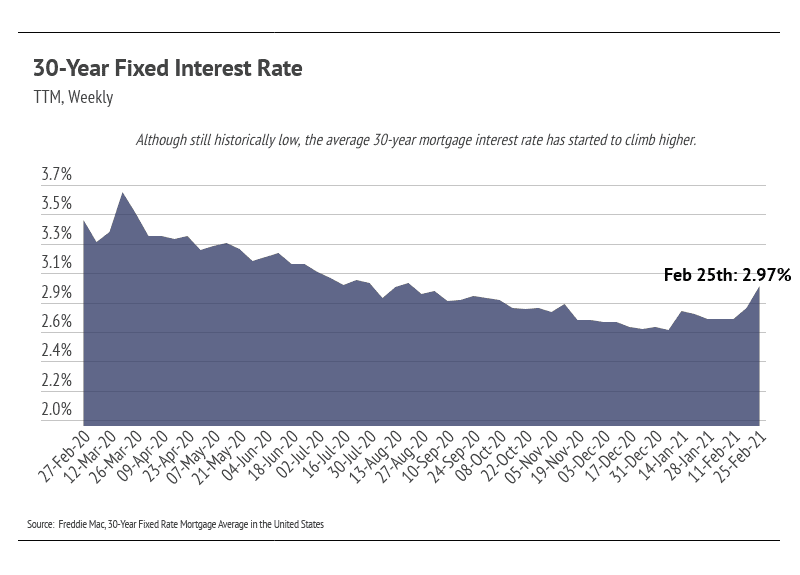

Over the last 12 months, mortgage interest rates fell, hitting all-time lows in December 2020 at 2.66%, and demand skyrocketed. Typically, if all other factors are equal, a 1% drop in interest rates allows a buyer to afford a 13% higher price in terms of monthly payment. For example, a person paying 4% on a $1,000,000 mortgage pays the same amount each month as a person with a $1,130,000 mortgage at 3%. In California, the drop in interest rates caused a buying frenzy, dropping the already-low housing supply even lower.

Mortgage rates are starting to rise, although they still remain quite low by any historical standard, which will generally have an adverse affect on affordability. Affordability decreases as mortgage rates increase, because a 1% increase makes a home 13% less affordable on a monthly payment basis. Usually, demand would also decrease, which it is likely to do, to some extent; however, California is so undersupplied that it won’t matter. We may be at the start of an unusual dynamic of rising rates and rising home prices, which will drop affordability further.

Although we don’t expect the same level of buying in 2021 as we saw in 2020, the environment is right for demand to outpace supply. In the short term, we may even see a demand spike as those able to buy try to purchase before rates rise higher. We anticipate a competitive landscape for buyers over the course of this year.

Conversely, now is an exceptional time to sell your home. Low inventory means multiple offers and fewer concessions. Our only note is that sellers are often selling one home and buying another, which makes working with the right agent even more important.

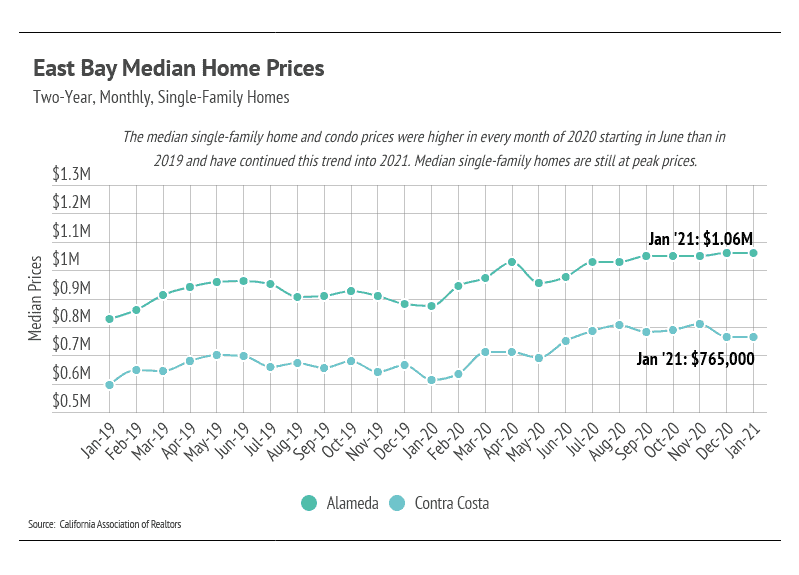

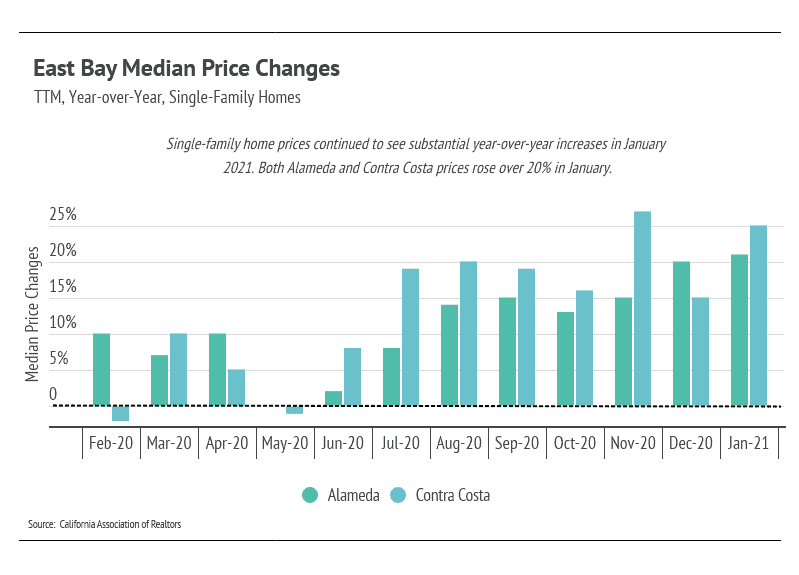

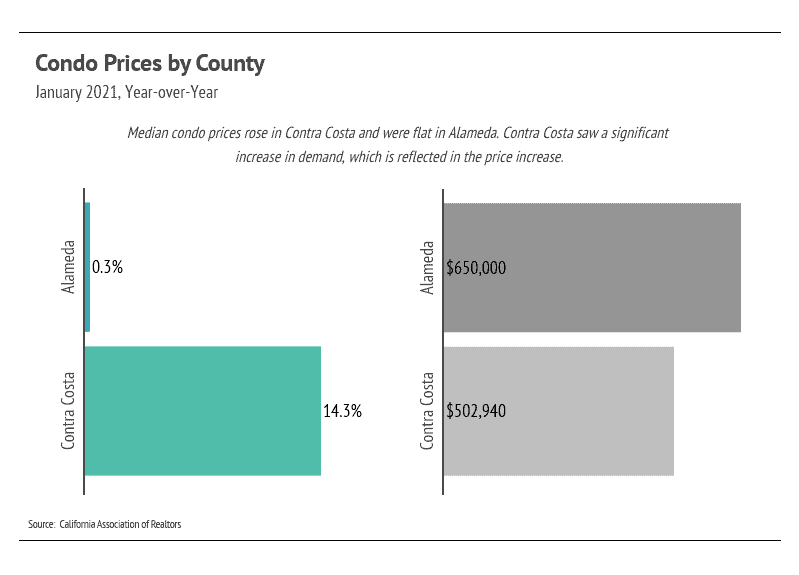

The median single-family home price and condo prices were flat month-over-month. Prices have remained quite stable over the last 12 months. Year-over-year, single-family home prices rose considerably in both Alameda and Contra Costa.

As you can see in the graph below, median condo prices were mixed. Alameda condo prices were flat relative to last January while Contra Costa condos experienced significant price appreciation.

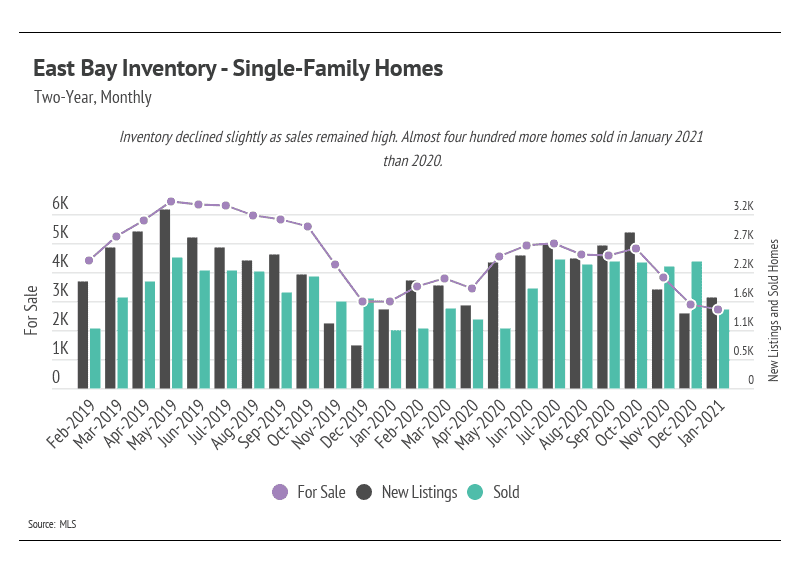

Single-family home inventory remained lower through 2020 relative to 2019 and dropped even further in January 2021, which speaks to the desirability of the East Bay area. During the pandemic, fewer people wanted to leave, and more people wanted to move to the area. New listings were lower than normal throughout the year, while sales were much higher. Sales in the autumn of 2020 were more substantial than the year before, and inventory is slightly lower than last year. Demand is still high in the area, and we expect prices to continue to appreciate throughout 2021.

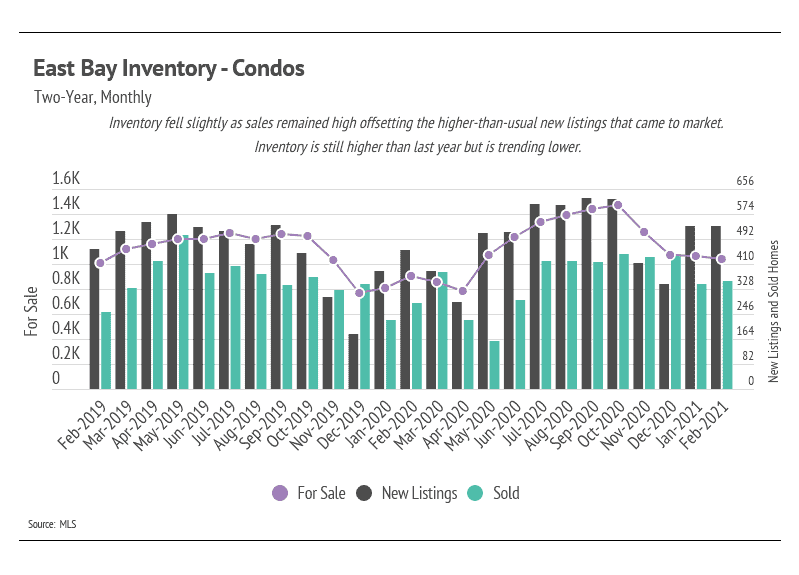

Like single-family homes, the number of condos on the market declined, but not to last year’s levels. Condo prices have shown stability despite higher inventory.

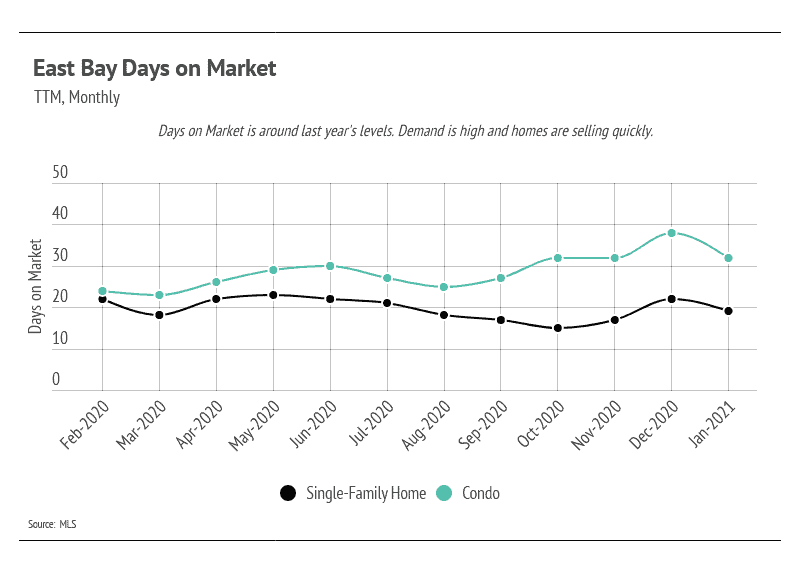

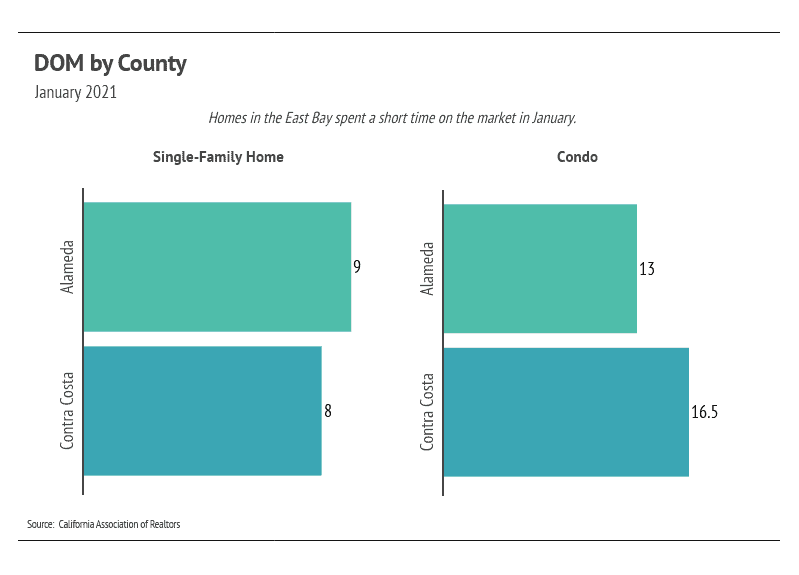

For single-family homes and condos, Days on Market (DOM) is trending upward, but both are still selling relatively quickly.

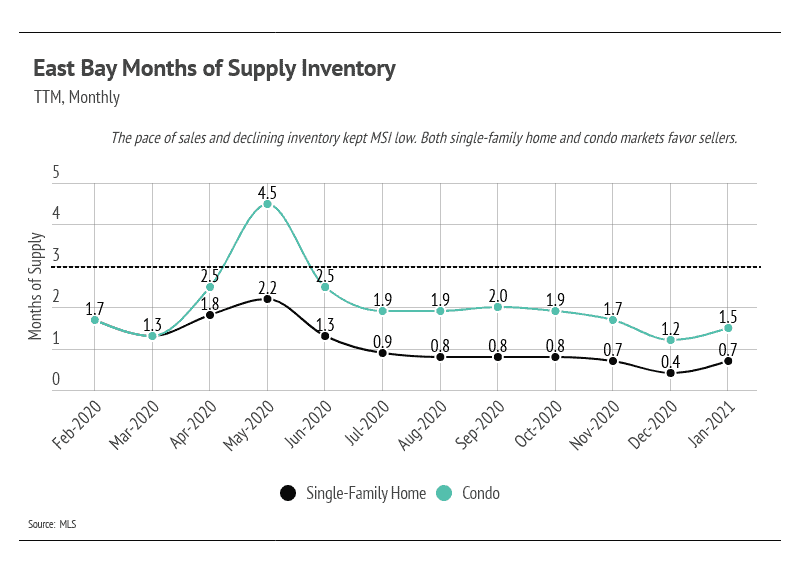

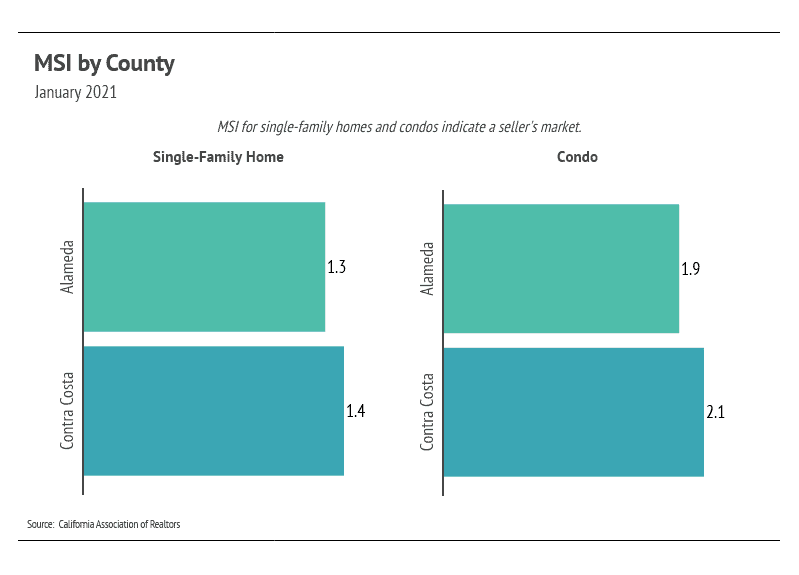

We can use MSI as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California (far lower than the national average of six months), which indicates a balanced market. An MSI lower than three means that there are more buyers than sellers on the market (i.e., it is a sellers’ market), while a higher MSI means there are more sellers than buyers (i.e., it is a buyers’ market). In January 2021, the MSI remained below two months of supply for both single-family homes and condos, favoring sellers.

In summary, the high demand and low supply present in East Bay has buoyed home prices. Inventory for single-family homes and condos will likely decline further this year, and fewer sellers will likely come to market, which will potentially lift prices higher. Overall, the housing market has shown its resilience through the pandemic and remains one of the most valuable asset classes. The data show that housing has remained consistently strong through this period.

We anticipate new listings to slow until around March 2021. While the winter season tends to see a slowdown in activity, January 2021 showed higher-than-normal sales, once again highlighting the desirability of East Bay.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

Stay up to date on the latest real estate trends.

Michelle Kim | July 17, 2026

Discover the strategies that help San Francisco homes stand out, attract serious buyers, and maximize value before they even hit the market.

Michelle Kim | July 10, 2026

Avoid the most common mistakes homeowners make before listing their property and learn how preparation, pricing, and marketing can help you achieve a successful home s… Read more

Michelle Kim | July 6, 2026

Learn the key factors that help San Francisco homes attract multiple offers, from strategic pricing and professional marketing to home presentation and buyer demand.

Michelle Kim | July 1, 2026

Quick Take: Prices are rising across much of the Bay Area, with San Francisco single-family homes breaching the $2.2 million mark for the first time and the East Bay p… Read more

Michelle Kim | July 1, 2026

Quick Take: Median sale prices posted gains in three of four counties, with Sonoma County leading the way at 2.33% year-over-year growth, while Marin County saw a 4.70… Read more

Michelle Kim | July 1, 2026

Quick Take: Prices are on the rise across the board, with single-family homes and condos both posting year-over-year gains for the first time in over a year. Inventory… Read more

You’ve got questions and we can’t wait to answer them.