South Bay & Peninsula Real Estate Market Report: January 2022

robyn January 3, 2022

robyn January 3, 2022

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

| Inflation: Short-lived or long-term? |

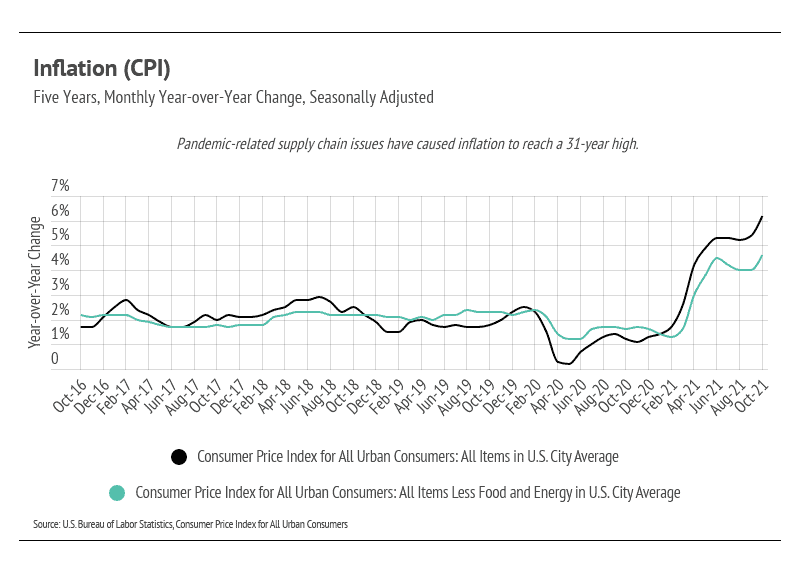

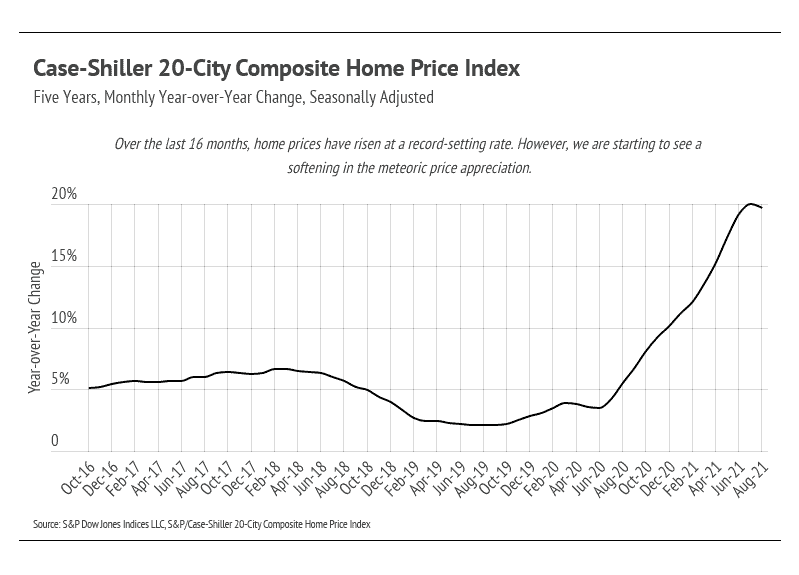

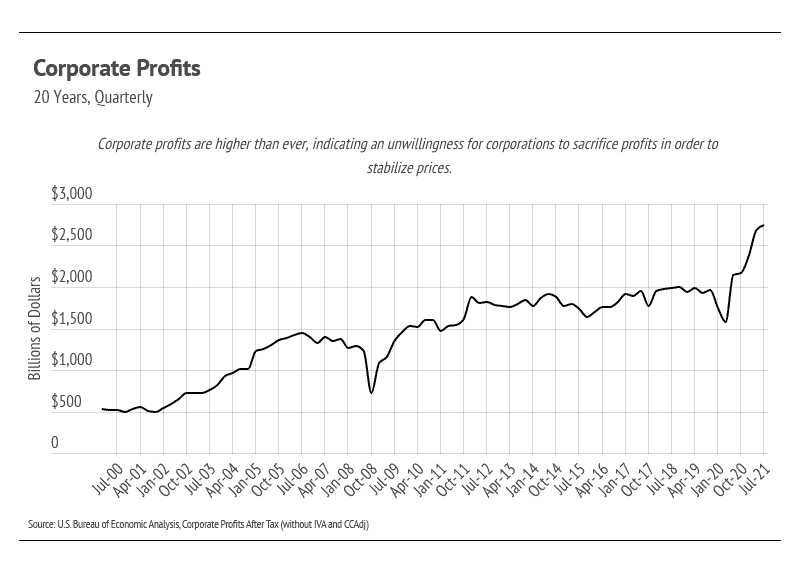

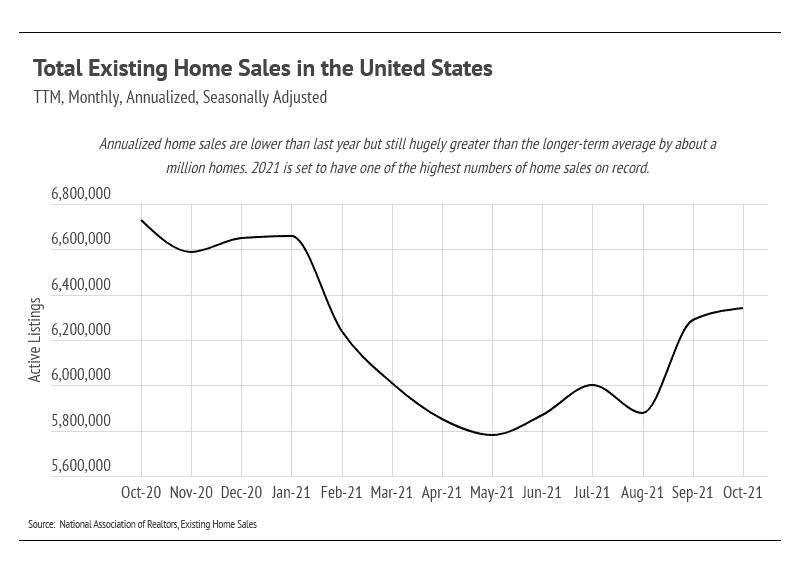

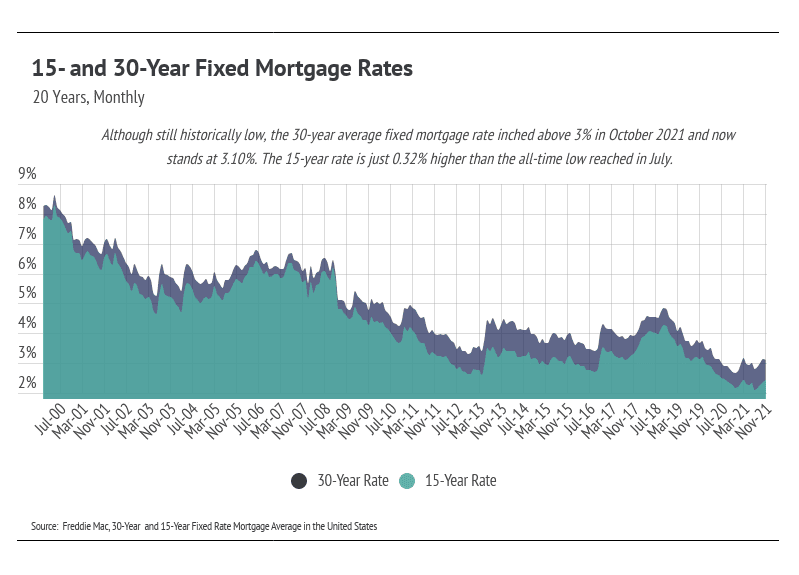

| By now, you’ve likely run across a headline regarding the large inflation jump we’ve experienced over the past six months. Even if you haven’t, you’ve probably noticed a general increase in prices for things like gas and food over the past couple of months. The last significant long-term inflationary period was in the 1970s when inflation expectations created a feedback loop largely because unions were common and had more bargaining power. As prices rose, union workers demanded higher pay, which increased operating costs and fueled rising prices. But 2020-21 is quite different from the 1970s. Currently, companies are using inflation as a mostly bad-faith excuse to raise prices during a time of record corporate profits, which will benefit companies as consumers bear the burden of rising costs. This is likely the unfortunate feedback loop we will see during the next six months. All that to say, as consumer costs rise, we might see demand for housing decline. With fewer experiences to spend money on during the pandemic, savings shot up, allowing potential homebuyers to reach their down payment goals far more quickly than expected. Inflation will cut into our ability to save. Unlike a normal business cycle, the pandemic is still disrupting the global supply chain, with fewer dock/port workers and truck drivers as well as continued international travel restrictions. This is compounded by the pandemic-related shifts in consumer preferences: consumers are choosing physical goods rather than services. The demand for physical goods isn’t unique to the U.S., either — the whole world is trying to recover economically with a move toward physical goods, which is stressing the supply chain. The good news, however, is that inflation will likely fall around summer 2022 and shouldn’t mimic the decade-long inflationary period of the 1970s. The bad news is that it isn’t coming down today. Although not necessarily a strict supply chain issue, the rising cost of housing can definitely be tied to supply. In the U.S., the supply of houses for sale is still near the all-time low reached in April. At the same time, demand remains high for homes, and we are on pace to have around a million more homes sold in 2021 than in a typical year, based on the long-term average. In other words, more homes are selling despite the historically low inventory. Because inflation diminishes the purchasing power of a dollar over time, buyers face pressure to buy sooner rather than later, further increasing demand for homes. Coupling inflation with historically low mortgage rates creates incentives to buy now even with the run-up in prices. The market remains competitive for buyers, but conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly. |

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

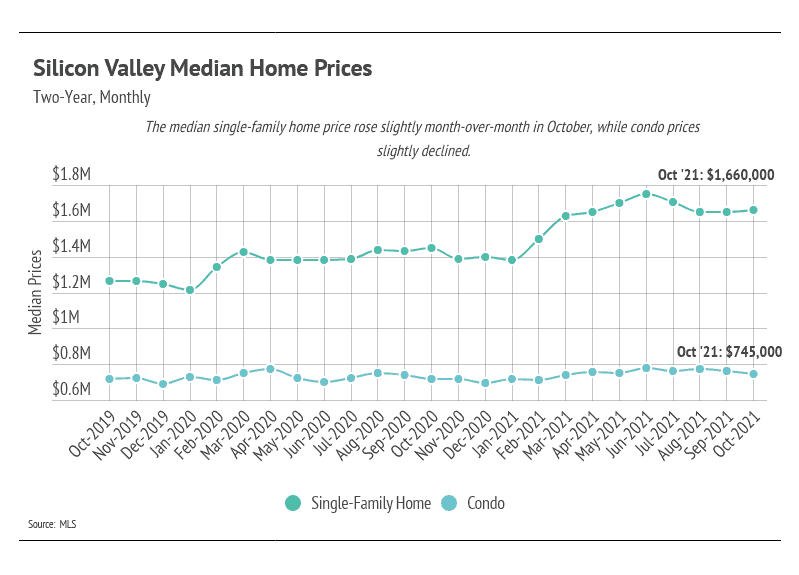

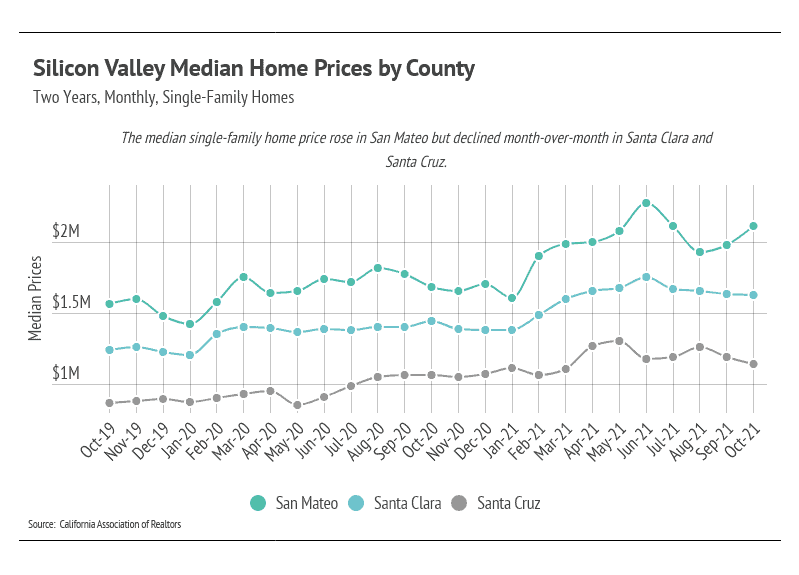

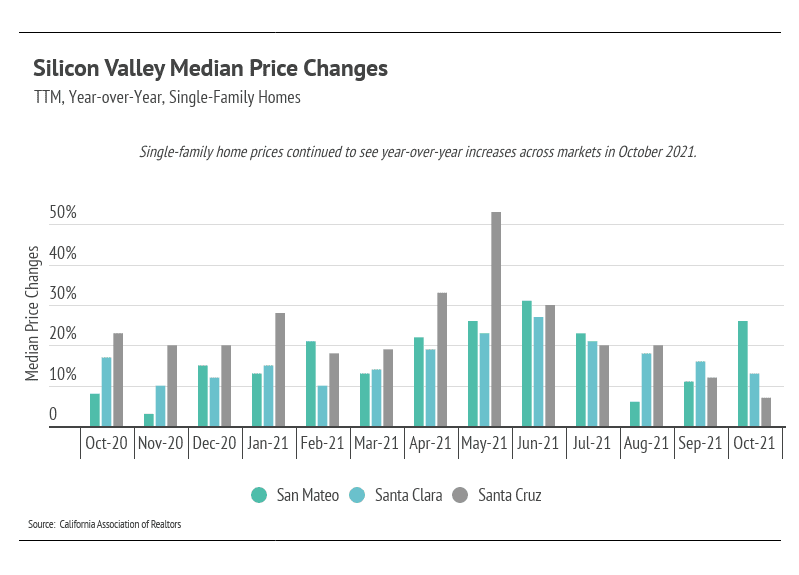

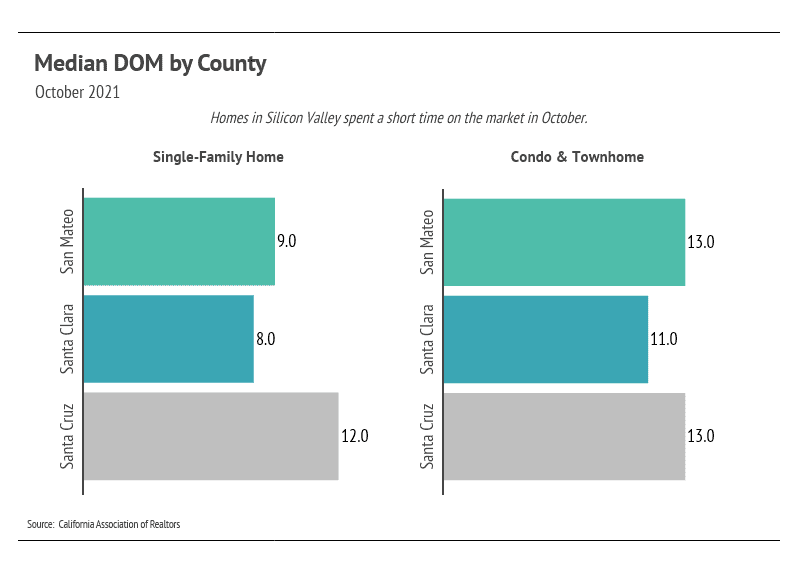

After single-family home prices appreciated significantly in the first half of the year, it makes sense that prices are declining in the third and fourth quarters except for San Mateo, whose prices have moved higher over the past two months. Although no market is at an all-time high in October, Silicon Valley home prices remain historically high. We expect price appreciation to decline through the winter, a seasonal norm.

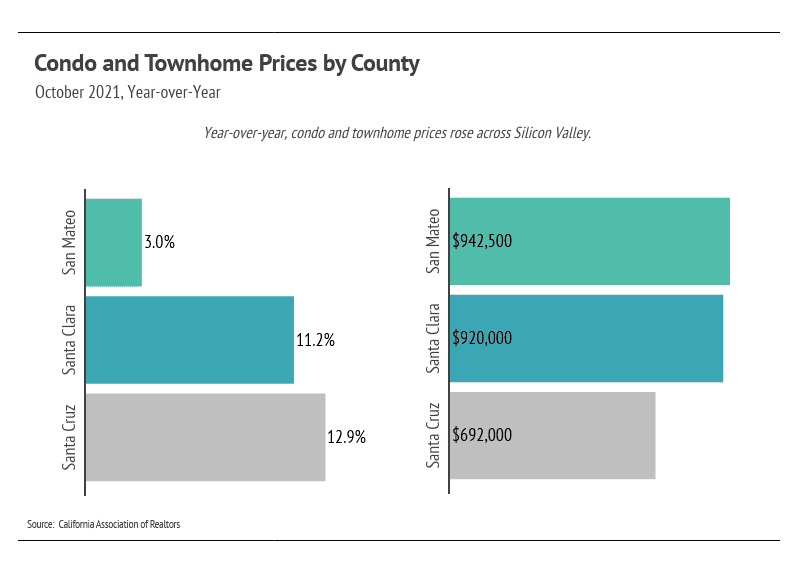

Condo prices are near all-time highs in Silicon Valley. Similar to single-family homes, prices contracted in the back half of the year. Although the price appreciation wasn’t as pronounced for condos as it was for single-family homes, the growth rates for condos in 2021 are still significant.

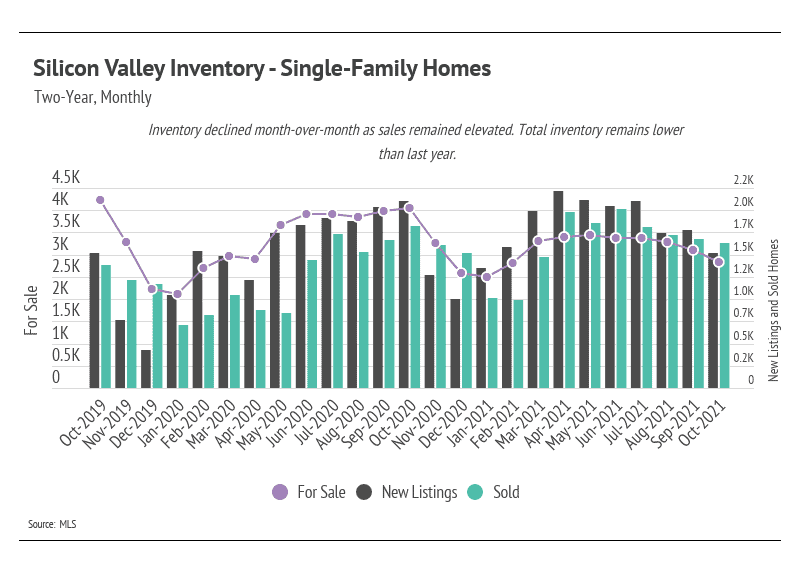

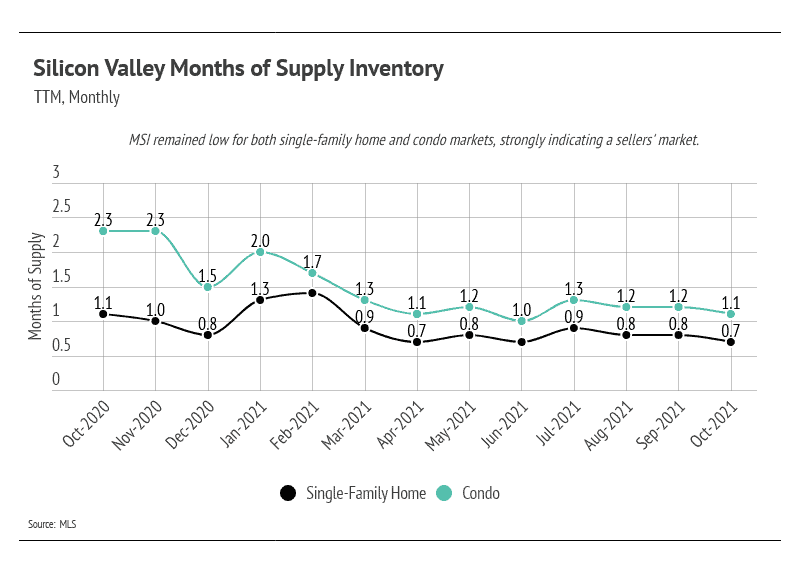

Despite the increase in single-family home inventory in 2021, we’re still at a historic low. August and September are typically the months each year with the highest inventory. In 2021, total inventory didn’t come close to last year’s level and was even further away from pre-pandemic levels. Even though we’re seeing some price correction after the first half of the year, the sustained low inventory will lift prices. Sales in Silicon Valley have been incredibly high, again highlighting demand in the area.

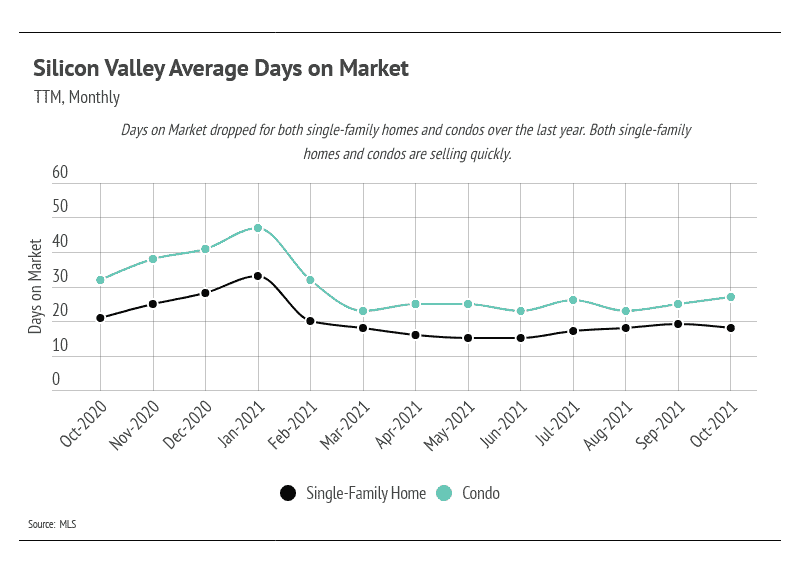

Homes are selling faster than at any point in the past 15 years. The Days on Market reflects the high demand for homes in Silicon Valley. Buyers must put in competitive offers, which, on average, are 1–5% above the list price of the home.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes for sale on the market to sell at the current rate of sales. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSIs in Silicon Valley are near all-time lows for single-family homes and condos, indicating a sellers’ market all around.

Stay up to date on the latest real estate trends.

Michelle Kim | May 29, 2026

A closer look at why more San Francisco buyers are prioritizing walkability, local cafés, restaurants, parks, and lifestyle when choosing the right neighborhood.

Michelle Kim | May 22, 2026

A closer look at how buyers are comparing condos and single-family homes in the 2026 San Francisco housing market based on lifestyle, budget, and long-term goals.

Michelle Kim | May 15, 2026

A closer look at why San Francisco buyers continue to prioritize neighborhoods near Golden Gate Park for outdoor access, walkability, and long-term livability.

Michelle Kim | May 8, 2026

A look at how Mosaik Real Estate supports Bay Area buyers and sellers through multilingual communication and local market expertise.

Michelle Kim | May 1, 2026

A closer look at San Francisco housing market trends in 2026 and what buyers and sellers should expect moving forward.

Michelle Kim | May 1, 2026

Quick Take: Median home sale prices ticked up slightly on both a month-over-month and year-over-year basis in February, continuing the holding pattern we've seen in re… Read more

You’ve got questions and we can’t wait to answer them.